UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended June 30, 2016

OR

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Cheniere Energy Partners, L.P.

(Exact name of registrant as specified in its charter)

|

| | |

Delaware | 001-33366 | 20-5913059 |

(State or other jurisdiction of incorporation or organization) | (Commission File Number) | (I.R.S. Employer Identification No.) |

| | |

700 Milam Street, Suite 1900 Houston, Texas | | 77002 |

(Address of principal executive offices) | | (Zip Code) |

(713) 375-5000

(Registrant’s telephone number, including area code) Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

| |

Large accelerated filer x | Accelerated filer o |

Non-accelerated filer o | Smaller reporting company o |

(Do not check if a smaller reporting company) |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

As of August 1, 2016, the issuer had 57,104,348 common units, 145,333,334 Class B units and 135,383,831 subordinated units outstanding.

CHENIERE ENERGY PARTNERS, L.P.

TABLE OF CONTENTS

DEFINITIONS

As commonly used in the liquefied natural gas industry, to the extent applicable and as used in this quarterly report, the terms listed below have the following meanings:

Common Industry and Other Terms

|

| | |

Bcf | | billion cubic feet |

Bcf/d | | billion cubic feet per day |

Bcf/yr | | billion cubic feet per year |

Bcfe | | billion cubic feet equivalent |

DOE | | U.S. Department of Energy |

EPC | | engineering, procurement and construction |

FERC | | Federal Energy Regulatory Commission |

FTA countries | | countries with which the United States has a free trade agreement providing for national treatment for trade in natural gas |

GAAP | | generally accepted accounting principles in the United States |

Henry Hub | | the final settlement price (in USD per MMBtu) for the New York Mercantile Exchange’s Henry Hub natural gas futures contract for the month in which a relevant cargo’s delivery window is scheduled to begin |

LIBOR | | London Interbank Offered Rate |

LNG | | liquefied natural gas, a product of natural gas consisting primarily of methane (CH4) that is in liquid form at near atmospheric pressure |

MMBtu | | million British thermal units, an energy unit |

mtpa | | million tonnes per annum |

non-FTA countries | | countries with which the United States does not have a free trade agreement providing for national treatment for trade in natural gas and with which trade is permitted |

SEC | | Securities and Exchange Commission |

SPA | | LNG sale and purchase agreement |

Train | | an industrial facility comprised of a series of refrigerant compressor loops used to cool natural gas into LNG |

TUA | | terminal use agreement |

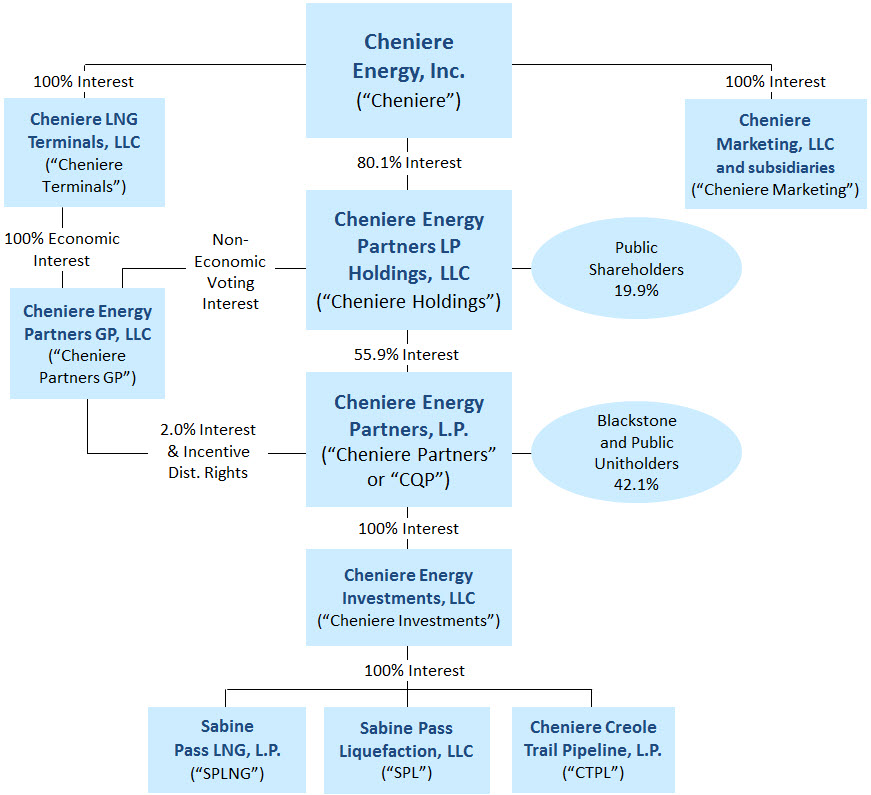

Abbreviated Organizational Structure

The following diagram depicts our abbreviated organizational structure as of June 30, 2016, including our ownership of certain subsidiaries, and the references to these entities used in this quarterly report:

Unless the context requires otherwise, references to “Cheniere Partners,” “the Partnership,” “we,” “us” and “our” refer to Cheniere Energy Partners, L.P. (NYSE MKT: CQP) and its consolidated subsidiaries, including SPLNG, SPL and CTPL.

References to “Blackstone Group” refer to The Blackstone Group, L.P. References to “Blackstone CQP Holdco” refer to Blackstone CQP Holdco LP. References to “Blackstone” refer to Blackstone Group and Blackstone CQP Holdco.

| |

PART I. | FINANCIAL INFORMATION |

| |

ITEM 1. | CONSOLIDATED FINANCIAL STATEMENTS |

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

(in thousands, except unit data)

|

| | | | | | | | |

| | June 30, | | December 31, |

| | 2016 | | 2015 |

ASSETS | | (unaudited) | | |

Current assets | | | | |

Cash and cash equivalents | | $ | 12,262 |

| | $ | 146,221 |

|

Restricted cash | | 450,506 |

| | 274,557 |

|

Accounts and other receivables | | 71,499 |

| | 741 |

|

Accounts receivable—affiliate | | 176 |

| | 1,271 |

|

Advances to affiliate | | 41,486 |

| | 39,836 |

|

Inventory | | 48,331 |

| | 16,667 |

|

Other current assets | | 21,726 |

| | 14,182 |

|

Total current assets | | 645,986 |

| | 493,475 |

|

| | | | |

Non-current restricted cash | | 13,650 |

| | 13,650 |

|

Property, plant and equipment, net | | 13,223,191 |

| | 11,931,602 |

|

Debt issuance costs, net | | 137,605 |

| | 132,091 |

|

Non-current derivative assets | | 20,472 |

| | 30,304 |

|

Other non-current assets | | 217,946 |

| | 232,031 |

|

Total assets | | $ | 14,258,850 |

| | $ | 12,833,153 |

|

| | | | |

LIABILITIES AND PARTNERS’ EQUITY | | | | |

Current liabilities | | | | |

Accounts payable | | $ | 35,581 |

| | $ | 16,407 |

|

Accrued liabilities | | 336,316 |

| | 224,292 |

|

Current debt, net | | 1,662,257 |

| | 1,673,379 |

|

Due to affiliates | | 87,349 |

| | 115,123 |

|

Deferred revenue | | 26,709 |

| | 26,669 |

|

Deferred revenue—affiliate | | 717 |

| | 717 |

|

Derivative liabilities | | 15,943 |

| | 6,430 |

|

Other current liabilities | | 54 |

| | — |

|

Total current liabilities | | 2,164,926 |

| | 2,063,017 |

|

| | | | |

Long-term debt, net | | 11,543,524 |

| | 10,018,325 |

|

Non-current deferred revenue | | 7,500 |

| | 9,500 |

|

Non-current derivative liabilities | | 26,904 |

| | 2,884 |

|

Other non-current liabilities | | 170 |

| | 175 |

|

Other non-current liabilities—affiliate | | 27,404 |

| | 26,321 |

|

| | | | |

Partners’ equity | | | | |

Common unitholders’ interest (57.1 million units issued and outstanding at June 30, 2016 and December 31, 2015) | | 204,009 |

| | 305,747 |

|

Class B unitholders’ interest (145.3 million units issued and outstanding at June 30, 2016 and December 31, 2015) | | (29,425 | ) | | (37,429 | ) |

Subordinated unitholders’ interest (135.4 million units issued and outstanding at June 30, 2016 and December 31, 2015) | | 301,749 |

| | 428,035 |

|

General partner’s interest (2% interest with 6.9 million units issued and outstanding at June 30, 2016 and December 31, 2015) | | 12,089 |

| | 16,578 |

|

Total partners’ equity | | 488,422 |

|

| 712,931 |

|

Total liabilities and partners’ equity | | $ | 14,258,850 |

| | $ | 12,833,153 |

|

The accompanying notes are an integral part of these consolidated financial statements.

3

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS

(in thousands, except per unit data)

(unaudited)

|

| | | | | | | | | | | | | | | | |

| | Three Months Ended June 30, | | Six Months Ended June 30, |

| | 2016 | | 2015 | | 2016 | | 2015 |

Revenues | |

| |

| | | | |

Regasification revenues | | $ | 65,122 |

| | $ | 66,490 |

| | $ | 130,506 |

| | $ | 133,208 |

|

Regasification revenues—affiliate | | 717 |

| | 1,199 |

| | 2,352 |

| | 2,011 |

|

LNG revenues | | 85,332 |

| | — |

| | 85,360 |

| | — |

|

Total revenues | | 151,171 |

| | 67,689 |

| | 218,218 |

| | 135,219 |

|

| | | | | | | | |

Operating costs and expenses | | |

| | | | | | |

Cost of sales (excluding depreciation and amortization expense shown separately below) | | 49,294 |

| | 91 |

| | 53,198 |

| | 784 |

|

Operating and maintenance expense | | 24,717 |

| | 9,298 |

| | 42,102 |

| | 39,838 |

|

Operating and maintenance expense—affiliate | | 11,156 |

| | 7,501 |

| | 21,986 |

| | 12,274 |

|

Development expense | | 70 |

| | 1,367 |

| | 136 |

| | 2,518 |

|

Development expense—affiliate | | 153 |

| | 206 |

| | 282 |

| | 410 |

|

General and administrative expense | | 3,792 |

| | 4,081 |

| | 6,402 |

| | 7,596 |

|

General and administrative expense—affiliate | | 21,211 |

| | 33,472 |

| | 43,409 |

| | 55,069 |

|

Depreciation and amortization expense | | 28,184 |

| | 15,991 |

| | 47,572 |

| | 30,870 |

|

Total operating costs and expenses | | 138,577 |

| | 72,007 |

| | 215,087 |

| | 149,359 |

|

| | | | | | | | |

Income (loss) from operations | | 12,594 |

| | (4,318 | ) | | 3,131 |

| | (14,140 | ) |

| | | | | | | | |

Other income (expense) | | |

| | | | | | |

Interest expense, net of capitalized interest | | (71,999 | ) | | (50,148 | ) | | (115,451 | ) | | (92,993 | ) |

Loss on early extinguishment of debt | | (26,304 | ) | | (7,281 | ) | | (27,761 | ) | | (96,273 | ) |

Derivative gain (loss), net | | (14,792 | ) | | 1,469 |

| | (35,600 | ) | | (35,669 | ) |

Other income | | 376 |

| | 235 |

| | 650 |

| | 356 |

|

Total other expense | | (112,719 | ) | | (55,725 | ) | | (178,162 | ) | | (224,579 | ) |

| | | | | | | | |

Net loss | | $ | (100,125 | ) | | $ | (60,043 | ) | | $ | (175,031 | ) | | $ | (238,719 | ) |

| | | | | | | | |

Basic and diluted net loss per common unit | | $ | (0.21 | ) | | $ | (0.01 | ) | | $ | (0.29 | ) | | $ | (0.62 | ) |

| | | | | | | | |

Weighted average number of common units outstanding used for basic and diluted net loss per common unit calculation | | 57,084 |

| | 57,080 |

| | 57,084 |

| | 57,080 |

|

The accompanying notes are an integral part of these consolidated financial statements.

4

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF PARTNERS’ EQUITY

(in thousands)

(unaudited)

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Common Unitholders’ Interest | | Class B Unitholders’ Interest | | Subordinated Unitholder’s Interest | | General Partner’s Interest | | Total Partners’ Equity |

| Units | | Amount | | Units | | Amount | | Units | | Amount | | Units | | Amount | |

Balance at December 31, 2015 | 57,084 |

| | $ | 305,747 |

| | 145,333 |

| | $ | (37,429 | ) | | 135,384 |

| | $ | 428,035 |

| | 6,894 |

| | $ | 16,578 |

| | $ | 712,931 |

|

Net loss | — |

| | (50,875 | ) | | — |

| | — |

| | — |

| | (120,656 | ) | | — |

| | (3,500 | ) | | (175,031 | ) |

Distributions | — |

| | (48,521 | ) | | — |

| | — |

| | — |

| | — |

| | — |

| | (990 | ) | | (49,511 | ) |

Issuance of common units as compensation to non-management directors | 1 |

| | 32 |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 1 |

| | 33 |

|

Amortization of beneficial conversion feature of Class B units | — |

| | (2,374 | ) | | — |

| | 8,004 |

| | — |

| | (5,630 | ) | | — |

| | — |

| | — |

|

Balance at June 30, 2016 | 57,085 |

| | $ | 204,009 |

| | 145,333 |

| | $ | (29,425 | ) | | 135,384 |

| | $ | 301,749 |

| | 6,894 |

| | $ | 12,089 |

| | $ | 488,422 |

|

The accompanying notes are an integral part of these consolidated financial statements.

5

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS

(in thousands)

(unaudited)

|

| | | | | | | |

| Six Months Ended June 30, |

| 2016 | | 2015 |

Cash flows from operating activities | | | |

Net loss | $ | (175,031 | ) | | $ | (238,719 | ) |

Adjustments to reconcile net loss to net cash provided by operating activities: | | | |

Non-cash LNG inventory write-downs | — |

| | 17,366 |

|

Depreciation and amortization expense | 47,572 |

| | 30,870 |

|

Amortization of debt issuance costs and discount | 8,873 |

| | 5,019 |

|

Loss on early extinguishment of debt | 27,761 |

| | 96,273 |

|

Total losses on derivatives, net | 47,696 |

| | 35,128 |

|

Net cash used for settlement of derivative instruments | (4,081 | ) | | (38,028 | ) |

Other | 33 |

| | 25 |

|

Changes in restricted cash for certain operating activities | 110,089 |

| | 15,954 |

|

Changes in operating assets and liabilities: | | | |

Accounts and other receivables | (70,757 | ) | | (77 | ) |

Accounts receivable—affiliate | 1,206 |

| | 1,441 |

|

Advances to affiliate | 956 |

| | 2,541 |

|

Inventory | (17,470 | ) | | (27,427 | ) |

Accounts payable and accrued liabilities | 49,320 |

| | 84,580 |

|

Due to affiliates | (2,955 | ) | | 12,627 |

|

Deferred revenue | (1,960 | ) | | (1,985 | ) |

Other, net | (8,737 | ) | | (9,509 | ) |

Other, net—affiliate | (751 | ) | | 16,501 |

|

Net cash provided by operating activities | 11,764 |

| | 2,580 |

|

| | | |

Cash flows from investing activities | |

| | |

|

Property, plant and equipment, net | (1,223,969 | ) | | (1,427,603 | ) |

Use of restricted cash for the acquisition of property, plant and equipment | 1,255,607 |

| | 1,471,632 |

|

Other | (38,782 | ) | | (51,017 | ) |

Net cash used in investing activities | (7,144 | ) | | (6,988 | ) |

| | | |

Cash flows from financing activities | |

| | |

|

Proceeds from issuances of debt | 3,365,000 |

| | 2,000,000 |

|

Repayments of debt | (1,842,305 | ) | | — |

|

Debt issuance and deferred financing costs | (70,049 | ) | | (145,998 | ) |

Investment in restricted cash | (1,541,645 | ) | | (1,854,002 | ) |

Distributions to owners | (49,511 | ) | | (49,508 | ) |

Other | (69 | ) | | — |

|

Net cash used in financing activities | (138,579 | ) | | (49,508 | ) |

| | | |

Net decrease in cash and cash equivalents | (133,959 | ) | | (53,916 | ) |

Cash and cash equivalents—beginning of period | 146,221 |

| | 248,830 |

|

Cash and cash equivalents—end of period | $ | 12,262 |

| | $ | 194,914 |

|

The accompanying notes are an integral part of these consolidated financial statements.

6

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

NOTE 1—BASIS OF PRESENTATION

The accompanying unaudited Consolidated Financial Statements of Cheniere Partners have been prepared in accordance with GAAP for interim financial information and with Rule 10-01 of Regulation S-X. Accordingly, they do not include all of the information and footnotes required by GAAP for complete financial statements. In our opinion, all adjustments, consisting only of normal recurring adjustments necessary for a fair presentation, have been included. Certain reclassifications have been made to conform prior period information to the current presentation. The reclassifications had no effect on our overall consolidated financial position, operating results or cash flows.

In 2016, we started production at our natural gas liquefaction facilities at the Sabine Pass LNG terminal (the “Liquefaction Project”). As a result, we introduced a new line item entitled “Cost of sales” and modified the components of activity included in “Operating and maintenance expense” on our Consolidated Statements of Operations. To conform to the new presentation, reclassifications were made to the prior periods. Cost of sales includes costs incurred directly for the production and delivery of LNG from the Liquefaction Project such as natural gas feedstock, variable transportation and storage costs, derivative gains and losses associated with economic hedges to secure natural gas feedstock for the Liquefaction Project, and other related costs to convert natural gas into LNG, all to the extent not utilized for the commissioning process. These costs were reclassified from operating and maintenance expense. Operating and maintenance expense now includes costs associated with operating and maintaining the Liquefaction Project such as third-party service and maintenance contract costs, payroll and benefit costs of operations personnel, natural gas transportation and storage capacity demand charges, derivative gains and losses related to the sale and purchase of LNG associated with the regasification terminal, insurance and regulatory costs.

Additionally, we distinguished and reclassified our historical “revenues” line item into “regasification revenues” and “LNG revenues.” Regasification revenues include LNG regasification capacity reservation fees that are received pursuant to our TUAs and tug services fees that are received by Sabine Pass Tug Services, LLC, a wholly owned subsidiary of SPLNG. Substantially all of our regasification revenues are received from our two long-term TUA customers. LNG revenues include fees that are received pursuant to our SPAs and related LNG marketing activities. During the three and six months ended June 30, 2016, we received substantially all of our net LNG revenues from one SPA customer.

Results of operations for the three and six months ended June 30, 2016 are not necessarily indicative of the operating results that will be realized for the year ending December 31, 2016.

We are not subject to either federal or state income tax, as our partners are taxed individually on their allocable share of our taxable income.

For further information, refer to the Consolidated Financial Statements and accompanying notes included in our annual report on Form 10-K for the year ended December 31, 2015.

NOTE 2—UNITHOLDERS’ EQUITY

The common units, Class B units and subordinated units represent limited partner interests in us. The holders of the units are entitled to participate in partnership distributions and exercise the rights and privileges available to limited partners under our partnership agreement. Our partnership agreement requires that, within 45 days after the end of each quarter, we distribute all of our available cash (as defined in our partnership agreement). Generally, our available cash is our cash on hand at the end of a quarter less the amount of any reserves established by our general partner. All distributions paid to date have been made from operating surplus as defined in the partnership agreement.

The holders of common units have the right to receive initial quarterly distributions of $0.425 per common unit, plus any arrearages thereon, before any distribution is made to the holders of the subordinated units. The holders of subordinated units will receive distributions only to the extent we have available cash above the initial quarterly distribution requirement for our common unitholders and general partner and certain reserves. Subordinated units will convert into common units on a one-for-one basis when we meet financial tests specified in the partnership agreement. Although common and subordinated unitholders are not obligated to fund losses of the Partnership, their capital accounts, which would be considered in allocating the net assets of the Partnership were it to be liquidated, continue to share in losses.

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

The general partner interest is entitled to at least 2% of all distributions made by us. In addition, the general partner holds incentive distribution rights, which allow the general partner to receive a higher percentage of quarterly distributions of available cash from operating surplus after the initial quarterly distributions have been achieved and as additional target levels are met. The higher percentages range from 15% to 50%.

During 2012, Blackstone CQP Holdco and Cheniere completed their purchases of a new class of equity interests representing limited partner interests in us (“Class B units”) for total consideration of $1.5 billion and $500.0 million, respectively. Proceeds from the financings were used to fund a portion of the costs of developing, constructing and placing into service the first two Trains of the Liquefaction Project. In May 2013, Cheniere purchased an additional 12.0 million Class B units for consideration of $180.0 million in connection with our acquisition of CTPL and Cheniere Pipeline GP Interests, LLC. In 2013, Cheniere formed Cheniere Holdings to hold its limited partner interests in us. The Class B units are subject to conversion, mandatorily or at the option of the Class B unitholders under specified circumstances, into a number of common units based on the then-applicable conversion value of the Class B units. The Class B units are not entitled to cash distributions except in the event of our liquidation or a merger, consolidation or other combination of us with another person or the sale of all or substantially all of our assets. On a quarterly basis beginning on the date of the initial purchase date of the Class B units, the conversion value of the Class B units increases at a compounded rate of 3.5% per quarter, subject to additional upward adjustment for certain equity and debt financings. The accreted conversion ratio of the Class B units owned by Cheniere Holdings and Blackstone CQP Holdco was 1.74 and 1.71, respectively, as of June 30, 2016. We expect the Class B units to mandatorily convert into common units within 90 days of the substantial completion date of Train 3 of the Liquefaction Project, which we currently expect to occur before June 30, 2017. If the Class B units are not mandatorily converted by July 2019, the holders of the Class B units have the option to convert the Class B units into common units at that time.

NOTE 3—RESTRICTED CASH

Restricted cash consists of funds that are contractually restricted as to usage or withdrawal and have been presented separately from cash and cash equivalents on our Consolidated Balance Sheets. As of June 30, 2016 and December 31, 2015, restricted cash consisted of the following (in thousands):

|

| | | | | | | | |

| | June 30, | | December 31, |

| | 2016 | | 2015 |

Current restricted cash | | | | |

SPLNG debt service and interest payment | | $ | 77,415 |

| | $ | 77,415 |

|

Liquefaction Project | | 263,114 |

| | 189,260 |

|

CTPL construction and interest payment | | — |

| | 7,882 |

|

CQP and cash held by guarantor subsidiaries | | 109,977 |

| | — |

|

Total current restricted cash | | $ | 450,506 |

| | $ | 274,557 |

|

| | | | |

Non-current restricted cash | | | | |

SPLNG debt service | | $ | 13,650 |

| | $ | 13,650 |

|

Under the indentures governing the senior notes issued by SPLNG (the “SPLNG Indentures”), except for permitted tax distributions, SPLNG may not make distributions until certain conditions are satisfied, including: (1) there must be on deposit in an interest payment account an amount equal to one-sixth of the semi-annual interest payment multiplied by the number of elapsed months since the last semi-annual interest payment, and (2) there must be on deposit in a permanent debt service reserve fund an amount equal to one semi-annual interest payment. Distributions are permitted only after satisfying the foregoing funding requirements, a fixed charge coverage ratio test of 2:1 and other conditions specified in the SPLNG Indentures. During the six months ended June 30, 2016 and 2015, SPLNG made distributions of $145.3 million and $199.6 million, respectively, after satisfying all the applicable conditions in the SPLNG Indentures.

In February 2016, we entered into a $2.8 billion credit facility (the “2016 CQP Credit Facilities”). We, and Cheniere Investments and CTPL as our guarantor subsidiaries, are subject to limitations on the use of cash under the terms of the 2016 CQP Credit Facilities and the related depositary agreement governing the extension of credit to us. Specifically, we, Cheniere Investments and CTPL may only withdraw funds from collateral accounts held at a designated depositary bank on a monthly basis and for specific purposes, including for the payment of operating expenses. In addition, distributions and capital expenditures may only be made quarterly and are subject to certain restrictions.

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

NOTE 4—ACCOUNTS AND OTHER RECEIVABLES

As of June 30, 2016 and December 31, 2015, accounts and other receivables consisted of the following (in thousands):

|

| | | | | | | | |

| | June 30, | | December 31, |

| | 2016 | | 2015 |

SPL trade receivable | | $ | 67,266 |

| | $ | — |

|

Interest receivable | | 116 |

| | 23 |

|

Other accounts receivable | | 4,117 |

| | 718 |

|

Total accounts and other receivables | | $ | 71,499 |

| | $ | 741 |

|

Pursuant to the accounts agreement entered into with the collateral trustee for the benefit of SPL’s debt holders, SPL is required to deposit all cash received into reserve accounts controlled by the collateral trustee. The usage or withdrawal of such cash is restricted to the payment of liabilities related to the Liquefaction Project and other restricted payments. As of June 30, 2016, the entire balance of the SPL trade receivable was from a single SPA customer.

NOTE 5—INVENTORY

As of June 30, 2016 and December 31, 2015, inventory consisted of the following (in thousands):

|

| | | | | | | | |

| | June 30, | | December 31, |

| | 2016 | | 2015 |

Natural gas | | $ | 5,338 |

| | $ | 5,724 |

|

LNG | | 17,535 |

| | 3,690 |

|

Materials and other | | 25,458 |

| | 7,253 |

|

Total inventory | | $ | 48,331 |

| | $ | 16,667 |

|

NOTE 6—PROPERTY, PLANT AND EQUIPMENT

Property, plant and equipment consists of LNG terminal costs and fixed assets, as follows (in thousands):

|

| | | | | | | | |

| | June 30, | | December 31, |

| | 2016 | | 2015 |

LNG terminal costs | | | | |

LNG terminal | | $ | 5,447,566 |

| | $ | 2,478,036 |

|

LNG terminal construction-in-process | | 8,224,575 |

| | 9,859,836 |

|

LNG site and related costs, net | | 131 |

| | 135 |

|

Accumulated depreciation | | (454,967 | ) | | (411,907 | ) |

Total LNG terminal costs, net | | 13,217,305 |

| | 11,926,100 |

|

Fixed assets | | |

| | |

|

Computer and office equipment | | 1,451 |

| | 1,126 |

|

Furniture and fixtures | | 1,667 |

| | 1,375 |

|

Computer software | | 4,457 |

| | 4,238 |

|

Machinery and equipment | | 1,938 |

| | 1,906 |

|

Vehicles | | 2,748 |

| | 2,081 |

|

Other | | 95 |

| | 93 |

|

Accumulated depreciation | | (6,470 | ) | | (5,317 | ) |

Total fixed assets, net | | 5,886 |

| | 5,502 |

|

Property, plant and equipment, net | | $ | 13,223,191 |

| | $ | 11,931,602 |

|

During the three and six months ended June 30, 2016, we realized offsets to LNG terminal costs of $128.1 million and $142.3 million, respectively, that were related to the sale of commissioning cargoes because these amounts were earned prior to the start of commercial operations, during the testing phase for the construction of Train 1 of the Liquefaction Project.

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

NOTE 7—DERIVATIVE INSTRUMENTS

We have entered into the following derivative instruments that are reported at fair value:

| |

• | interest rate swaps to hedge the exposure to volatility in a portion of the floating-rate interest payments under certain of our credit facilities (“Interest Rate Derivatives”); |

| |

• | commodity derivatives consisting of natural gas purchase agreements for the commissioning and operation of the Liquefaction Project (“Physical Liquefaction Supply Derivatives”) and associated economic hedges (“Financial Liquefaction Supply Derivatives”, and collectively with the Physical Liquefaction Supply Derivatives, the “Liquefaction Supply Derivatives”); and |

| |

• | commodity derivatives to hedge the exposure to price risk attributable to future: (1) sales of our LNG inventory and (2) purchases of natural gas to operate the Sabine Pass LNG terminal (“Natural Gas Derivatives”). |

None of our derivative instruments are designated as cash flow hedging instruments, and changes in fair value are recorded within our Consolidated Statements of Operations.

SPLNG has elected to account for a portion of the Natural Gas Derivatives as normal purchase normal sale transactions, exempt from fair value accounting. Gains and losses for these physical hedges are not reflected on our Consolidated Statements of Operations until the period of delivery. SPLNG had not posted collateral for such forward contracts as of June 30, 2016 and December 31, 2015.

The following table (in thousands) shows the fair value of our derivative instruments that are required to be measured at fair value on a recurring basis as of June 30, 2016 and December 31, 2015, which are classified as other current assets, non-current derivative assets, derivative liabilities or non-current derivative liabilities in our Consolidated Balance Sheets.

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Fair Value Measurements as of |

| June 30, 2016 | | December 31, 2015 |

| Quoted Prices in Active Markets (Level 1) | | Significant Other Observable Inputs (Level 2) | | Significant Unobservable Inputs (Level 3) | | Total | | Quoted Prices in Active Markets (Level 1) | | Significant Other Observable Inputs (Level 2) | | Significant Unobservable Inputs (Level 3) | | Total |

SPL Interest Rate Derivatives liability | $ | — |

| | $ | (20,666 | ) | | $ | — |

| | $ | (20,666 | ) | | $ | — |

| | $ | (8,740 | ) | | $ | — |

| | $ | (8,740 | ) |

CQP Interest Rate Derivatives liability | — |

| | (19,148 | ) | | — |

| | (19,148 | ) | | — |

| | — |

| | — |

| | — |

|

Liquefaction Supply Derivatives asset (liability) | (2,850 | ) | | 381 |

| | 22,434 |

| | 19,965 |

| | — |

| | (25 | ) | | 32,492 |

| | 32,467 |

|

Natural Gas Derivatives asset | — |

| | — |

| | — |

| | — |

| | — |

| | 39 |

| | — |

| | 39 |

|

We value our Interest Rate Derivatives using valuations based on the initial trade prices. Using an income-based approach, subsequent valuations are based on observable inputs to the valuation model including interest rate curves, risk adjusted discount rates, credit spreads and other relevant data. The estimated fair values of our Natural Gas Derivatives are the amounts at which the instruments could be exchanged currently between willing parties. We value these derivatives using observable commodity price curves and other relevant data.

The fair value of substantially all of our Physical Liquefaction Supply Derivatives is developed through the use of internal models which are impacted by inputs that are unobservable in the marketplace. As a result, the fair value of our Physical Liquefaction Supply Derivatives is designated as Level 3 within the valuation hierarchy. The curves used to generate the fair value of our Physical Liquefaction Supply Derivatives are based on basis adjustments applied to forward curves for a liquid trading point. In addition, there may be observable liquid market basis information in the near term, but terms of a particular Physical Liquefaction Supply Derivatives contract may exceed the period for which such information is available, resulting in a Level 3 classification. In these instances, the fair value of the contract incorporates extrapolation assumptions made in the determination of the market basis price for future delivery periods in which applicable commodity basis prices were either not observable or lacked corroborative market data. Internal fair value models include conditions precedent to the respective long-term natural gas purchase agreements. As of June 30, 2016 and December 31, 2015, some of our Physical Liquefaction Supply Derivatives existed within markets for which the pipeline infrastructure is under development to accommodate marketable physical gas flow. Accordingly, our internal

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

fair value models are based on market prices that equate to our own contractual pricing due to: (1) the inactive and unobservable market and (2) conditions precedent and their impact on the uncertainty in the timing of our actual receipt of the physical volumes associated with each forward. The fair value of our Physical Liquefaction Supply Derivatives is predominantly driven by market commodity basis prices and our assessment of the associated conditions precedent, including evaluating whether the respective market is available as pipeline infrastructure is developed. Upon the completion and placement into service of relevant pipeline infrastructure to accommodate marketable physical gas flow, we recognize a gain or loss based on the fair value of the respective natural gas purchase agreements as of the reporting date.

As all of our Physical Liquefaction Supply Derivatives are either purely index-priced or index-priced with a fixed basis, we do not believe that a significant change in market commodity prices would have a material impact on our Level 3 fair value measurements. The following table includes quantitative information for the unobservable inputs for our Level 3 Physical Liquefaction Supply Derivatives as of June 30, 2016:

|

| | | | | | | | |

| | Net Fair Value Asset (in thousands) | | Valuation Technique | | Significant Unobservable Input | | Significant Unobservable Inputs Range |

Physical Liquefaction Supply Derivatives | | $22,434 | | Income Approach | | Basis Spread | | $(0.35) - $(0.02) |

The following table (in thousands) shows the changes in the fair value of our Level 3 Physical Liquefaction Supply Derivatives during the three and six months ended June 30, 2016 and 2015:

|

| | | | | | | | | | | | | | | | |

| | Three Months Ended June 30, | | Six Months Ended June 30, |

| | 2016 | | 2015 | | 2016 | | 2015 |

Balance, beginning of period | | $ | 30,054 |

| | $ | 342 |

| | $ | 32,492 |

| | $ | 342 |

|

Realized and mark-to-market losses: | | | | | | | | |

Included in cost of sales (1) | | (7,855 | ) | | 27 |

| | (10,204 | ) | | 27 |

|

Purchases and settlements: | | | | | | | | |

Purchases | | (16 | ) | | 71 |

| | 31 |

| | 71 |

|

Settlements (1) | | (71 | ) | | — |

| | (128 | ) | | — |

|

Transfers out of Level 3 (2) | | 322 |

| | — |

| | 243 |

| | — |

|

Balance, end of period | | $ | 22,434 |

| | $ | 440 |

| | $ | 22,434 |

| | $ | 440 |

|

Change in unrealized gains relating to instruments still held at end of period | | $ | (7,795 | ) | | $ | 27 |

| | $ | (9,484 | ) | | $ | 27 |

|

| |

(1) | Does not include the decrease in fair value of $0.1 million and $0.7 million related to the realized gains capitalized during the three and six months ended June 30, 2016, respectively. |

| |

(2) | Transferred to Level 2 as a result of observable market for the underlying natural gas purchase agreements. |

Derivative assets and liabilities arising from our derivative contracts with the same counterparty are reported on a net basis, as all counterparty derivative contracts provide for net settlement. The use of derivative instruments exposes us to counterparty credit risk, or the risk that a counterparty will be unable to meet its commitments in instances when our derivative instruments are in an asset position.

Interest Rate Derivatives

SPL Interest Rate Derivatives

SPL has entered into interest rate swaps (“SPL Interest Rate Derivatives”) to protect against volatility of future cash flows and hedge a portion of the variable interest payments on the credit facilities it entered into in June 2015 (the “2015 SPL Credit Facilities”). The SPL Interest Rate Derivatives hedge a portion of the expected outstanding borrowings over the term of the 2015 SPL Credit Facilities.

In March 2015, SPL settled a portion of the SPL Interest Rate Derivatives and recognized a derivative loss of $34.7 million within our Consolidated Statements of Operations in conjunction with the termination of approximately $1.8 billion of commitments under the previous credit facilities.

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

CQP Interest Rate Derivatives

In March 2016, we entered into interest rate swaps (“CQP Interest Rate Derivatives”) to protect against volatility of future cash flows and hedge a portion of the variable interest payments on the 2016 CQP Credit Facilities. The CQP Interest Rate Derivatives hedge a portion of the expected outstanding borrowings over the term of the 2016 CQP Credit Facilities.

As of June 30, 2016, we had the following Interest Rate Derivatives outstanding:

|

| | | | | | | | | | | | |

| | Initial Notional Amount | | Maximum Notional Amount | | Effective Date | | Maturity Date | | Weighted Average Fixed Interest Rate Paid | | Variable Interest Rate Received |

SPL Interest Rate Derivatives | | $20.0 million | | $628.8 million | | August 14, 2012 | | July 31, 2019 | | 1.98% | | One-month LIBOR |

CQP Interest Rate Derivatives | | $225.0 million | | $1.3 billion | | March 22, 2016 | | February 29, 2020 | | 1.19% | | One-month LIBOR |

The following table (in thousands) shows the fair value and location of our Interest Rate Derivatives on our Consolidated Balance Sheets:

|

| | | | | | | | | | | | | | | | | | | | | | | | |

| | June 30, 2016 | | December 31, 2015 |

| | SPL Interest Rate Derivatives | | CQP Interest Rate Derivatives | | Total | | SPL Interest Rate Derivatives | | CQP Interest Rate Derivatives | | Total |

Balance Sheet Location | | | | | | | | | | | | |

Derivative liabilities | | $ | (7,340 | ) | | $ | (5,570 | ) | | $ | (12,910 | ) | | $ | (5,940 | ) | | $ | — |

| | $ | (5,940 | ) |

Non-current derivative liabilities | | (13,326 | ) | | (13,578 | ) | | (26,904 | ) | | (2,800 | ) | | — |

| | (2,800 | ) |

Total derivative liabilities | | $ | (20,666 | ) | | $ | (19,148 | ) | | $ | (39,814 | ) | | $ | (8,740 | ) | | $ | — |

| | $ | (8,740 | ) |

The following table (in thousands) shows the changes in the fair value and settlements of our Interest Rate Derivatives recorded in derivative gain (loss), net on our Consolidated Statements of Operations during the three and six months ended June 30, 2016 and 2015:

|

| | | | | | | | | | | | | | | | |

| | Three Months Ended June 30, | | Six Months Ended June 30, |

| | 2016 | | 2015 | | 2016 | | 2015 |

SPL Interest Rate Derivatives gain (loss) | | $ | (4,752 | ) | | $ | 1,469 |

| | $ | (16,030 | ) | | $ | (35,669 | ) |

CQP Interest Rate Derivatives loss | | (10,040 | ) | | — |

| | (19,570 | ) | | — |

|

Commodity Derivatives

Liquefaction Supply Derivatives

SPL has entered into index-based physical natural gas supply contracts and associated economic hedges to purchase natural gas for the commissioning and operation of the Liquefaction Project. The terms of the physical natural gas supply contracts primarily range from approximately one to seven years and commence upon the satisfaction of certain conditions precedent, including but not limited to the date of first commercial operation of specified Trains of the Liquefaction Project. We recognize our Physical Liquefaction Supply Derivatives as either assets or liabilities and measure those instruments at fair value. Changes in the fair value of our Physical Liquefaction Supply Derivatives are reported in earnings. As of June 30, 2016, SPL has secured up to approximately 2,027.5 million MMBtu of natural gas feedstock through natural gas purchase agreements. The notional natural gas position of our Physical Liquefaction Supply Derivatives was approximately 1,114.5 million MMBtu as of June 30, 2016.

Our Financial Liquefaction Supply Derivatives are executed through over-the-counter contracts which are subject to nominal credit risk as these transactions are settled on a daily margin basis with investment grade financial institutions. We are required by these financial institutions to use margin deposits as credit support for our Financial Liquefaction Supply Derivatives activities.

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

Natural Gas Derivatives

Our Natural Gas Derivatives were executed through over-the-counter contracts which were subject to nominal credit risk as these transactions settled on a daily margin basis with investment grade financial institutions. We were required by these financial institutions to use margin deposits as credit support for our Natural Gas Derivatives activities. As of June 30, 2016, we did not have any open Natural Gas Derivatives positions or margin deposits at financial institutions.

We recognize all commodity derivative instruments that qualify for derivative accounting treatment, including our Liquefaction Supply Derivatives and our Natural Gas Derivatives (collectively, “Commodity Derivatives”), as either assets or liabilities and measure those instruments at fair value. Changes in the fair value of our Commodity Derivatives are reported in earnings.

The following table (in thousands) shows the fair value and location of our Commodity Derivatives on our Consolidated Balance Sheets:

|

| | | | | | | | | | | | | | | | | | | | | | | |

| June 30, 2016 | | December 31, 2015 |

| Liquefaction Supply Derivatives (1) | | Natural Gas Derivatives | | Total | | Liquefaction Supply Derivatives | | Natural Gas Derivatives (2) | | Total |

Balance Sheet Location | | | | | | | | | | | |

Other current assets | $ | 2,526 |

| | $ | — |

| | $ | 2,526 |

| | $ | 2,737 |

| | $ | 39 |

| | $ | 2,776 |

|

Non-current derivative assets | 20,472 |

| | — |

| | 20,472 |

| | 30,304 |

| | — |

| | 30,304 |

|

Total derivative assets | 22,998 |

| | — |

| | 22,998 |

| | 33,041 |

| | 39 |

| | 33,080 |

|

| | | | | | | | | | | |

Derivative liabilities | (3,033 | ) | | — |

| | (3,033 | ) | | (490 | ) | | — |

| | (490 | ) |

Non-current derivative liabilities | — |

| | — |

| | — |

| | (84 | ) | | — |

| | (84 | ) |

Total derivative liabilities | (3,033 | ) | | — |

| | (3,033 | ) | | (574 | ) | | — |

| | (574 | ) |

| | | | | | | | | | | |

Derivative asset, net | $ | 19,965 |

|

| $ | — |

| | $ | 19,965 |

| | $ | 32,467 |

| | $ | 39 |

| | $ | 32,506 |

|

| |

(1) | Does not include collateral of $0.5 million deposited for such contracts, which is included in other current assets in our Consolidated Balance Sheet as of June 30, 2016. |

| |

(2) | Does not include collateral of $0.4 million deposited for such contracts, which is included in other current assets in our Consolidated Balance Sheet as of December 31, 2015. |

The following table (in thousands) shows the changes in the fair value, settlements and location of our Commodity Derivatives recorded on our Consolidated Statements of Operations during the three and six months ended June 30, 2016 and 2015:

|

| | | | | | | | | | | | | | | | | |

| | | Three Months Ended June 30, | | Six Months Ended June 30, |

| Statement of Operations Location | | 2016 | | 2015 | | 2016 | | 2015 |

Liquefaction Supply Derivatives loss | LNG revenues | | $ | (34 | ) | | $ | — |

| | $ | (6 | ) | | $ | — |

|

Liquefaction Supply Derivatives gain (loss) (1) | Cost of sales | | (8,670 | ) | | 81 |

| | (12,264 | ) | | 81 |

|

Natural Gas Derivatives gain (loss) | Operating and maintenance expense | | — |

| | (294 | ) | | 174 |

| | 460 |

|

| |

(1) | Does not include the realized value associated with derivative instruments that settle through physical delivery. |

The use of Commodity Derivatives exposes us to counterparty credit risk, or the risk that a counterparty will be unable to meet its commitments in instances when our Commodity Derivatives are in an asset position.

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

Balance Sheet Presentation

Our derivative instruments are presented on a net basis on our Consolidated Balance Sheets as described above. The following table (in thousands) shows the fair value of our derivatives outstanding on a gross and net basis:

|

| | | | | | | | | | | | |

| | Gross Amounts Recognized | | Gross Amounts Offset in the Consolidated Balance Sheets | | Net Amounts Presented in the Consolidated Balance Sheets |

Offsetting Derivative Assets (Liabilities) | | | |

As of June 30, 2016 | | | | | | |

SPL Interest Rate Derivatives | | $ | (20,666 | ) | | $ | — |

| | $ | (20,666 | ) |

CQP Interest Rate Derivatives | | (19,148 | ) | | — |

| | (19,148 | ) |

Liquefaction Supply Derivatives | | 23,165 |

| | (167 | ) | | 22,998 |

|

Liquefaction Supply Derivatives | | (4,505 | ) | | 1,472 |

| | (3,033 | ) |

As of December 31, 2015 | | | | | | |

SPL Interest Rate Derivatives | | $ | (8,740 | ) | | $ | — |

| | $ | (8,740 | ) |

Liquefaction Supply Derivatives | | 33,636 |

| | (595 | ) | | 33,041 |

|

Liquefaction Supply Derivatives | | (574 | ) | | — |

| | (574 | ) |

Natural Gas Derivatives | | 188 |

| | (149 | ) | | 39 |

|

NOTE 8—OTHER NON-CURRENT ASSETS

As of June 30, 2016 and December 31, 2015, other non-current assets consisted of the following (in thousands):

|

| | | | | | | | |

| | June 30, | | December 31, |

| | 2016 | | 2015 |

Advances made under EPC and non-EPC contracts | | $ | 14,000 |

| | $ | 32,049 |

|

Advances made to municipalities for water system enhancements | | 95,584 |

| | 89,953 |

|

Tax-related payments and receivables | | 25,751 |

| | 27,615 |

|

Information technology service assets | | 29,532 |

| | 30,371 |

|

Other | | 53,079 |

| | 52,043 |

|

Total other non-current assets | | $ | 217,946 |

| | $ | 232,031 |

|

NOTE 9—ACCRUED LIABILITIES

As of June 30, 2016 and December 31, 2015, accrued liabilities consisted of the following (in thousands):

|

| | | | | | | | |

| | June 30, | | December 31, |

| | 2016 | | 2015 |

Interest costs and related debt fees | | $ | 155,222 |

| | $ | 150,336 |

|

Liquefaction Project costs | | 174,645 |

| | 67,006 |

|

LNG terminal costs | | 4,795 |

| | 3,918 |

|

Other accrued liabilities | | 1,654 |

| | 3,032 |

|

Total accrued liabilities | | $ | 336,316 |

| | $ | 224,292 |

|

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

NOTE 10—DEBT

As of June 30, 2016 and December 31, 2015, our debt consisted of the following (in thousands):

|

| | | | | | | | |

| | June 30, | | December 31, |

| | 2016 | | 2015 |

Long-term debt: | | | | |

SPLNG | | | | |

6.50% Senior Secured Notes due 2020 (“2020 SPLNG Senior Notes”) (1) | | $ | 420,000 |

| | $ | 420,000 |

|

SPL | | | | |

5.625% Senior Secured Notes due 2021 (“2021 SPL Senior Notes”), net of unamortized premium of $7,959 and $8,718 | | 2,007,959 |

| | 2,008,718 |

|

6.25% Senior Secured Notes due 2022 (“2022 SPL Senior Notes”) | | 1,000,000 |

| | 1,000,000 |

|

5.625% Senior Secured Notes due 2023 (“2023 SPL Senior Notes”), net of unamortized premium of $6,029 and $6,392 | | 1,506,029 |

| | 1,506,392 |

|

5.75% Senior Secured Notes due 2024 (“2024 SPL Senior Notes”) | | 2,000,000 |

| | 2,000,000 |

|

5.625% Senior Secured Notes due 2025 (“2025 SPL Senior Notes”) | | 2,000,000 |

| | 2,000,000 |

|

5.875% Senior Secured Notes due 2026 (“2026 SPL Senior Notes”) | | 1,500,000 |

| | — |

|

2015 SPL Credit Facilities | | 832,695 |

| | 845,000 |

|

CTPL | | | | |

$400.0 million Term Loan Facility (“CTPL Term Loan”), net of unamortized discount of zero and $1,429 | | — |

| | 398,571 |

|

Cheniere Partners | | | | |

2016 CQP Credit Facilities | | 450,000 |

| | — |

|

Unamortized debt issuance costs (2) | | (173,159 | ) | | (160,356 | ) |

Total long-term debt, net | | 11,543,524 |

| | 10,018,325 |

|

| | | | |

Current debt: | | | | |

7.50% Senior Secured Notes due 2016 (“2016 SPLNG Senior Notes”), net of unamortized discount of $1,956 and $4,303 (3) | | 1,663,544 |

| | 1,661,197 |

|

$1.2 billion SPL Working Capital Facility (“SPL Working Capital Facility”) | | — |

| | 15,000 |

|

Unamortized debt issuance costs (2) | | (1,287 | ) | | (2,818 | ) |

Total current debt, net | | 1,662,257 |

| | 1,673,379 |

|

| | | | |

Total debt, net | | $ | 13,205,781 |

| | $ | 11,691,704 |

|

| |

(1) | Must be redeemed or repaid concurrently with the 2016 SPLNG Senior Notes under the terms of the 2016 CQP Credit Facilities if the obligations under the 2016 SPLNG Senior Notes are satisfied with borrowings under the 2016 CQP Credit Facilities. |

| |

(2) | Effective January 1, 2016, we adopted ASU 2015-03 and ASU 2015-15, which require debt issuance costs related to term notes to be presented in the balance sheet as a direct deduction from the debt liability, rather than as an asset, retrospectively for each reporting period presented. As a result, we reclassified $160.4 million and $2.8 million from debt issuance costs, net to long-term debt, net and current debt, net, respectively, as of December 31, 2015. |

| |

(3) | Matures on November 30, 2016. We currently anticipate satisfying this obligation with borrowings under the 2016 CQP Credit Facilities. |

2016 Debt Issuances and Redemptions

2026 SPL Senior Notes

In June 2016, SPL issued an aggregate principal amount of $1.5 billion of the 2026 SPL Senior Notes. Net proceeds of the offering of approximately $1.3 billion, after deducting commissions, fees and expenses and incremental interest required under the 2026 SPL Senior Notes during construction, were used to prepay a portion of the outstanding borrowings under the 2015 SPL Credit Facilities, resulting in a write-off of debt issuance costs associated with the 2015 SPL Credit Facilities of $26.0 million during both the three and six months ended June 30, 2016. The 2026 SPL Senior Notes accrue interest at a fixed rate of 5.875%

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

and interest on the 2026 SPL Senior Notes is payable semi-annually in arrears. The terms of the 2026 SPL Senior Notes are governed by the same common indenture as SPL’s other senior notes, which contains customary terms and events of default, covenants and redemption terms.

In connection with the closing of the sale of the 2026 SPL Senior Notes, SPL entered into a Registration Rights Agreement dated June 14, 2016 (the “2026 SPL Registration Rights Agreement”). Under the terms of the 2026 SPL Registration Rights Agreement, SPL has agreed, and any future guarantors of the 2026 SPL Senior Notes will agree, to use commercially reasonable efforts to file with the SEC and cause to become effective a registration statement within 360 days after June 14, 2016 with respect to an offer to exchange any and all of the 2026 SPL Senior Notes for a like aggregate principal amount of debt securities of SPL with terms identical in all material respects to the respective 2026 SPL Senior Notes sought to be exchanged (other than with respect to restrictions on transfer or to any increase in annual interest rate), and that are registered under the Securities Act of 1933, as amended. Under specified circumstances, SPL has also agreed, and any future guarantors will also agree, to use commercially reasonable efforts to cause to become effective a shelf registration statement relating to resales of the 2026 SPL Senior Notes. SPL will be obligated to pay additional interest if it fails to comply with its obligation to register the 2026 SPL Senior Notes within the specified time period.

2016 CQP Credit Facilities

In February 2016, we entered into the $2.8 billion 2016 CQP Credit Facilities, which consist of: (1) a $450.0 million CTPL tranche term loan that was used to prepay the $400.0 million CTPL Term Loan in February 2016, (2) an approximately $2.1 billion SPLNG tranche term loan that will be used to redeem or repay the approximately $2.1 billion of the 2016 SPLNG Senior Notes and the 2020 SPLNG Senior Notes (which must be redeemed or repaid concurrently under the terms of the 2016 CQP Credit Facilities ), (3) a $125.0 million debt service reserve credit facility (the “DSR Facility”) that may be used to satisfy a six-month debt service reserve requirement and (4) a $115.0 million revolving credit facility that may be used for general business purposes.

The 2016 CQP Credit Facilities accrue interest at a variable rate per annum equal to LIBOR or the base rate (equal to the highest of the prime rate, the federal funds effective rate, as published by the Federal Reserve Bank of New York, plus 0.50% and adjusted one month LIBOR plus 1.0%), plus the applicable margin. The applicable margin for LIBOR loans is 2.25% per annum, and the applicable margin for base rate loans is 1.25% per annum, in each case with a 0.50% step-up beginning on February 25, 2019. Interest on LIBOR loans is due and payable at the end of each applicable LIBOR period (and at the end of every three month period within the LIBOR period, if any), and interest on base rate loans is due and payable at the end of each calendar quarter.

We incurred $48.7 million of debt issuance costs during the six months ended June 30, 2016, and will incur an additional $21.5 million of debt issuance costs when the SPLNG tranche is funded. The prepayment of the CTPL Term Loan resulted in a write-off of unamortized discount and debt issuance costs of $1.5 million during the six months ended June 30, 2016. We pay a commitment fee equal to an annual rate of 40% of the margin for LIBOR loans multiplied by the average daily amount of the undrawn commitment, payable quarterly in arrears. The DSR Facility and the revolving credit facility are both available for the issuance of letters of credit, which incur a fee equal to an annual rate of 2.25% of the undrawn portion with a 0.50% step-up beginning on February 25, 2019.

The 2016 CQP Credit Facilities mature on February 25, 2020, and the outstanding balance may be repaid, in whole or in part, at any time without premium or penalty, except for interest hedging and interest rate breakage costs. The 2016 CQP Credit Facilities contain conditions precedent for extensions of credit, as well as customary affirmative and negative covenants and limit our ability to make restricted payments, including distributions, to once per fiscal quarter as long as certain conditions are satisfied. Under the terms of the 2016 CQP Credit Facilities, we are required to hedge not less than 50% of the variable interest rate exposure on its projected aggregate outstanding balance, maintain a minimum debt service coverage ratio of at least 1.15x at the end of each fiscal quarter beginning March 31, 2019 and have a projected debt service coverage ratio of 1.55x in order to incur additional indebtedness to refinance a portion of the existing obligations.

The 2016 CQP Credit Facilities are unconditionally guaranteed by each of our subsidiaries other than: (1) SPL, (2) SPLNG until funding of its tranche term loan and (3) certain of our subsidiaries owning other development projects, as well as certain other specified subsidiaries and members of the foregoing entities.

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

Credit Facilities

Below is a summary of our credit facilities outstanding as of June 30, 2016 (in thousands):

|

| | | | | | | | | | | | |

| | 2015 SPL Credit Facilities | | SPL Working Capital Facility | | 2016 CQP Credit Facilities |

Original facility size | | $ | 4,600,000 |

| | $ | 1,200,000 |

| | $ | 2,800,000 |

|

Outstanding balance | | 832,695 |

| | — |

| | 450,000 |

|

Commitments terminated | | 1,287,305 |

| | — |

| | — |

|

Letters of credit issued | | — |

| | 237,270 |

| | 7,500 |

|

Available commitment | | $ | 2,480,000 |

| | $ | 962,730 |

| | $ | 2,342,500 |

|

| | | | | | |

Interest rate | | LIBOR plus 1.30% - 1.75% or base rate plus 1.75% | | LIBOR plus 1.75% or base rate plus 0.75% | | LIBOR plus 2.25% or base rate plus 1.25% (1) |

Maturity date | | Earlier of December 31, 2020 or second anniversary of SPL Trains 1 through 5 completion date | | December 31, 2020, with various terms for underlying loans | | February 25, 2020, with principals due quarterly commencing on February 19, 2019 |

| |

(1) | There is a 0.50% step-up for both LIBOR and base rate loans beginning on February 25, 2019. |

Interest Expense

Total interest expense consisted of the following (in thousands):

|

| | | | | | | | | | | | | | | | |

| | Three Months Ended June 30, | | Six Months Ended June 30, |

| | 2016 | | 2015 | | 2016 | | 2015 |

Total interest cost | | $ | 204,693 |

| | $ | 174,825 |

| | $ | 397,313 |

| | $ | 334,911 |

|

Capitalized interest | | (132,694 | ) | | (124,677 | ) | | (281,862 | ) | | (241,918 | ) |

Total interest expense, net | | $ | 71,999 |

| | $ | 50,148 |

| | $ | 115,451 |

| | $ | 92,993 |

|

Fair Value Disclosures

The following table (in thousands) shows the carrying amount and estimated fair value of our debt:

|

| | | | | | | | | | | | | | | | |

| | June 30, 2016 | | December 31, 2015 |

| | Carrying Amount | | Estimated Fair Value | | Carrying Amount | | Estimated Fair Value |

Senior Notes, net of premium or discount (1) | | $ | 12,097,532 |

| | $ | 12,163,254 |

| | $ | 10,596,307 |

| | $ | 9,525,809 |

|

CTPL Term Loan, net of discount (2) | | — |

| | — |

| | 398,571 |

| | 400,000 |

|

Credit facilities (2) (3) | | 1,282,695 |

| | 1,282,695 |

| | 860,000 |

| | 860,000 |

|

| |

(1) | Includes 2016 SPLNG Senior Notes, net of discount; 2020 SPLNG Senior Notes; 2021 SPL Senior Notes, net of premium; 2022 SPL Senior Notes; 2023 SPL Senior Notes, net of premium; 2024 SPL Senior Notes; 2025 SPL Senior Notes and 2026 SPL Senior Notes (collectively, the “Senior Notes”). The Level 2 estimated fair value was based on quotes obtained from broker-dealers or market makers of the Senior Notes and other similar instruments. |

| |

(2) | The Level 3 estimated fair value approximates the principal amount because the interest rates are variable and reflective of market rates and the debt may be repaid, in full or in part, at any time without penalty. |

| |

(3) | Includes 2015 SPL Credit Facilities, SPL Working Capital Facility and 2016 CQP Credit Facilities. |

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

NOTE 11—RELATED PARTY TRANSACTIONS

Below is a summary of our related party transactions as reported on our Consolidated Statements of Operations for the three and six months ended June 30, 2016 and 2015 (in thousands):

|

| | | | | | | | | | | | | | | | |

| Three Months Ended June 30, | | Six Months Ended June 30, |

| 2016 | | 2015 | | 2016 | | 2015 |

Regasification revenues—affiliate |

Contracts for Sale and Purchase of Natural Gas and LNG | $ | — |

| | $ | — |

| | $ | 919 |

| | $ | — |

|

Tug Boat Lease Sharing Agreement | 717 |

| | 708 |

| | 1,433 |

| | 1,417 |

|

Other agreements | — |

| | 491 |

| | — |

| | 594 |

|

Total regasification revenues—affiliate | 717 |

|

| 1,199 |

|

| 2,352 |

|

| 2,011 |

|

|

Operating and maintenance expense—affiliate |

Contracts for Sale and Purchase of Natural Gas and LNG | — |

| | — |

| | 607 |

| | — |

|

Services Agreements | 11,167 |

| | 7,502 |

| | 21,395 |

| | 12,280 |

|

Other agreements | (11 | ) | | (1 | ) | | (16 | ) | | (6 | ) |

Total operating and maintenance expense—affiliate | 11,156 |

|

| 7,501 |

|

| 21,986 |

|

| 12,274 |

|

|

Development expense—affiliate |

Services Agreements | 153 |

| | 206 |

| | 282 |

| | 410 |

|

|

General and administrative expense—affiliate |

Services Agreements | 21,211 |

| | 33,472 |

| | 43,409 |

| | 55,069 |

|

LNG Terminal Capacity Agreements

Terminal Use Agreements

SPL obtained approximately 2.0 Bcf/d of regasification capacity under a TUA with SPLNG as a result of an assignment in July 2012 by Cheniere Investments of its rights, title and interest under its TUA with SPLNG. SPL is obligated to make monthly capacity payments (the “TUA Fees”) to SPLNG aggregating approximately $250 million per year, continuing until at least 20 years after SPL delivers its first commercial cargo at the Liquefaction Project.

In connection with this TUA, SPL is required to pay for a portion of the cost (primarily LNG inventory) to maintain the cryogenic readiness of the regasification facilities at the Sabine Pass LNG terminal, which is recorded as operating and maintenance expense on our Consolidated Statements of Operations.

Cheniere Investments, SPL and SPLNG entered into the terminal use rights assignment and agreement (the “TURA”) pursuant to which Cheniere Investments has the right to use SPL’s reserved capacity under the TUA and has the obligation to pay the TUA Fees required by the TUA to SPLNG. However, the revenue earned by SPLNG from the TUA Fees and the loss incurred by Cheniere Investments under the TURA are eliminated upon consolidation of our Financial Statements. We have guaranteed the obligations of SPL under its TUA and the obligations of Cheniere Investments under the TURA.

In an effort to utilize Cheniere Investments’ reserved capacity under the TURA during construction of the Liquefaction Project, Cheniere Marketing has entered into an amended and restated variable capacity rights agreement with Cheniere Investments (the “Amended and Restated VCRA”) pursuant to which Cheniere Marketing is obligated to pay Cheniere Investments 80% of the expected gross margin of each cargo of LNG that Cheniere Marketing arranges for delivery to the Sabine Pass LNG terminal. Cheniere Investments recorded no revenues—affiliate from Cheniere Marketing during the three and six months ended June 30, 2016 and 2015, respectively, related to the Amended and Restated VCRA.

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

Cheniere Marketing SPA

Cheniere Marketing has entered into an SPA with SPL to purchase, at Cheniere Marketing’s option, any LNG produced by SPL in excess of that required for other customers at a price of 115% of Henry Hub plus $3.00 per MMBtu of LNG.

Commissioning Agreement

In May 2015, SPL entered into an agreement with Cheniere Marketing that obligates Cheniere Marketing in certain circumstances to buy LNG cargoes produced during the periods while Bechtel Oil, Gas and Chemicals, Inc. has control of, and is commissioning, the first four Trains of the Liquefaction Project.

Pre-commercial LNG Marketing Agreement

In May 2015, SPL entered into an agreement with Cheniere Marketing that authorizes Cheniere Marketing to act on SPL’s behalf to market and sell pre-commercial LNG that has not been accepted by BG Gulf Coast LNG, LLC.

Services Agreements

As of June 30, 2016 and December 31, 2015, we had $41.5 million and $39.8 million of advances to affiliates, respectively, under the services agreements described below. The non-reimbursement amounts incurred under the services agreements described below are recorded in general and administrative expense—affiliate.

Cheniere Partners Services Agreement

We have entered into a services agreement with Cheniere Terminals, a wholly owned subsidiary of Cheniere, pursuant to which Cheniere Terminals is entitled to a quarterly non-accountable overhead reimbursement charge of $2.8 million (adjusted for inflation) for the provision of various general and administrative services for our benefit. In addition, Cheniere Terminals is entitled to reimbursement for all audit, tax, legal and finance fees incurred by Cheniere Terminals that are necessary to perform the services under the agreement.

Cheniere Investments Information Technology Services Agreement

Cheniere Investments has entered into an information technology services agreement with Cheniere, pursuant to which Cheniere Investments’ subsidiaries receive certain information technology services. On a quarterly basis, the various entities receiving the benefit are invoiced by Cheniere according to the cost allocation percentages set forth in the agreement. In addition, Cheniere is entitled to reimbursement for all costs incurred by Cheniere that are necessary to perform the services under the agreement.

SPLNG O&M Agreement

SPLNG has entered into a long-term operation and maintenance agreement (the “SPLNG O&M Agreement”) with Cheniere Investments pursuant to which SPLNG receives all necessary services required to operate and maintain the Sabine Pass LNG receiving terminal. SPLNG incurs a fixed monthly fee of $130,000 (indexed for inflation) under the SPLNG O&M Agreement and the cost of a bonus equal to 50% of the salary component of labor costs in certain circumstances to be agreed upon between SPLNG and Cheniere Investments at the beginning of each operating year. In addition, SPLNG incurs costs to reimburse Cheniere Investments for its operating expenses, which consist primarily of labor expenses. Cheniere Investments provides the services required under the SPLNG O&M Agreement pursuant to a secondment agreement with a wholly owned subsidiary of Cheniere. All payments received by Cheniere Investments under the SPLNG O&M Agreement are required to be remitted to such subsidiary.

SPLNG MSA

SPLNG has entered into a long-term management services agreement (the “SPLNG MSA”) with Cheniere Terminals, pursuant to which Cheniere Terminals manages the operation of the Sabine Pass LNG receiving terminal, excluding those matters provided for under the SPLNG O&M Agreement. SPLNG incurs a monthly fixed fee of $520,000 (indexed for inflation) under the SPLNG MSA.

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

SPL O&M Agreement

SPL has entered into an operation and maintenance agreement (the “SPL O&M Agreement”) with Cheniere Investments pursuant to which SPL receives all of the necessary services required to construct, operate and maintain the Liquefaction Project. Before the Liquefaction Project is operational, the services to be provided include, among other services, obtaining governmental approvals on behalf of SPL, preparing an operating plan for certain periods, obtaining insurance, preparing staffing plans and preparing status reports. After the Liquefaction Project is operational, the services include all necessary services required to operate and maintain the Liquefaction Project. Before the Liquefaction Project is operational, in addition to reimbursement of operating expenses, SPL is required to pay a monthly fee equal to 0.6% of the capital expenditures incurred in the previous month. After substantial completion of each Train, for services performed while the Liquefaction Project is operational, SPL will pay, in addition to the reimbursement of operating expenses, a fixed monthly fee of $83,333 (indexed for inflation) for services with respect to such Train. Cheniere Investments provides the services required under the SPL O&M Agreement pursuant to a secondment agreement with a wholly owned subsidiary of Cheniere. All payments received by Cheniere Investments under the SPL O&M Agreement are required to be remitted to such subsidiary.

SPL MSA

SPL has entered into a management services agreement (the “SPL MSA”) with Cheniere Terminals pursuant to which Cheniere Terminals manages the construction and operation of the Liquefaction Project, excluding those matters provided for under the SPL O&M Agreement. The services include, among other services, exercising the day-to-day management of SPL’s affairs and business, managing SPL’s regulatory matters, managing bank and brokerage accounts and financial books and records of SPL’s business and operations, entering into financial derivatives on SPL’s behalf and providing contract administration services for all contracts associated with the Liquefaction Project. Under the SPL MSA, SPL pays a monthly fee equal to 2.4% of the capital expenditures incurred in the previous month. After substantial completion of each Train, SPL will pay a fixed monthly fee of $541,667 (indexed for inflation) for services with respect to such Train.

CTPL O&M Agreement

CTPL has entered into an amended long-term operation and maintenance agreement (the “CTPL O&M Agreement”) with Cheniere Investments pursuant to which CTPL receives all necessary services required to operate and maintain the Creole Trail Pipeline. CTPL is required to reimburse the counterparty for its operating expenses, which consist primarily of labor expenses. Cheniere Investments provides the services required under the CTPL O&M Agreement pursuant to a secondment agreement with a wholly owned subsidiary of Cheniere. All payments received by Cheniere Investments under the CTPL O&M Agreement are required to be remitted to such subsidiary.

CTPL MSA

CTPL has entered into a management services agreement (the “CTPL MSA”) with Cheniere Terminals pursuant to which Cheniere Terminals manages the modification and operation of the Creole Trail Pipeline, excluding those matters provided for under the CTPL O&M Agreement. The services include, among other services, exercising the day-to-day management of CTPL’s affairs and business, managing CTPL’s regulatory matters, managing bank and brokerage accounts and financial books and records of CTPL’s business and operations and providing contract administration services for all contracts associated with the pipeline facilities. Under the CTPL MSA, CTPL pays a monthly fee equal to 3.0% of the capital expenditures to enable bi-directional natural gas flow on the Creole Trail Pipeline incurred in the previous month.

LNG Lease Agreement

In September 2011, Cheniere Investments entered into an agreement in the form of a lease (the “LNG Lease Agreement”) with Cheniere Marketing that enables Cheniere Investments to supply the Sabine Pass LNG terminal with LNG to maintain proper LNG inventory levels and temperature. The LNG Lease Agreement also enables Cheniere Investments to hedge the exposure to variability in expected future cash flows of the LNG inventory. Under the terms of the LNG Lease Agreement, Cheniere Marketing funds all activities related to the purchase and hedging of the LNG, and Cheniere Investments reimburses Cheniere Marketing for all costs and assumes full price risk associated with these activities. As a result of Cheniere Investments assuming full price risk associated with the LNG Lease Agreement, any LNG inventory purchased by Cheniere Marketing under this arrangement is

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

classified as inventory—affiliate. As of June 30, 2016 and December 31, 2015, Cheniere Investments had no LNG inventory—affiliate recorded under the LNG Lease Agreement.

Agreement to Fund SPLNG’s Cooperative Endeavor Agreements (“CEAs”)

SPLNG has executed CEAs with various Cameron Parish, Louisiana taxing authorities that allowed them to collect certain annual property tax payments from SPLNG from 2007 through 2016. This ten-year initiative represented an aggregate commitment of $24.5 million in order to aid in their reconstruction efforts following Hurricane Rita, which SPLNG fulfilled its obligations in the first quarter of 2016. In exchange for SPLNG’s advance payments of annual ad valorem taxes, Cameron Parish will grant SPLNG a dollar-for-dollar credit against future ad valorem taxes to be levied against the Sabine Pass LNG terminal starting in 2019. Beginning in September 2007, SPLNG entered into various agreements with Cheniere Marketing, pursuant to which Cheniere Marketing would pay SPLNG additional TUA revenues equal to any and all amounts payable by SPLNG to the Cameron Parish taxing authorities under the CEAs. In exchange for such amounts received as TUA revenues from Cheniere Marketing, SPLNG will make payments to Cheniere Marketing equal to, and in the year the Cameron Parish dollar-for-dollar credit is applied against, ad valorem tax levied on our LNG terminal.

On a consolidated basis, these advance tax payments were recorded to other non-current assets, and payments from Cheniere Marketing that SPLNG utilized to make the ad valorem tax payments were recorded as a long-term obligation. As of June 30, 2016 and December 31, 2015, we had $24.5 million and $22.1 million, respectively, of both other non-current assets resulting from SPLNG’s ad valorem tax payments and non-current liabilities—affiliate resulting from these payments received from Cheniere Marketing.

Contracts for Sale and Purchase of Natural Gas and LNG

SPLNG is able to sell and purchase natural gas and LNG under agreements with Cheniere Marketing. Under these agreements, SPLNG purchases natural gas or LNG from Cheniere Marketing at a sales price equal to the actual purchase price paid by Cheniere Marketing to suppliers of the natural gas or LNG, plus any third-party costs incurred by Cheniere Marketing with respect to the receipt, purchase and delivery of natural gas or LNG to the Sabine Pass LNG terminal.

Tug Boat Lease Sharing Agreement

In connection with its tug boat lease, Sabine Pass Tug Services, LLC (“Tug Services”), a wholly owned subsidiary of SPLNG, entered into a tug sharing agreement with a wholly owned subsidiary of Cheniere to provide its LNG cargo vessels with tug boat and marine services at the Sabine Pass LNG terminal.

LNG Terminal Export Agreement