| |

ITEM 8. | FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA |

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

CHENIERE ENERGY PARTNERS, L.P.

Report of Independent Registered Public Accounting Firm

To the Unitholders of Cheniere Energy Partners, L.P. and

Board of Directors of Cheniere Energy Partners GP, LLC:

Opinion on the Consolidated Financial Statements

We have audited the accompanying consolidated balance sheets of Cheniere Energy Partners, L.P. and subsidiaries (the Partnership) as of December 31, 2017 and 2016, the related consolidated statements of operations, partners’ equity, and cash flows for each of the years in the three‑year period ended December 31, 2017, and the related notes (collectively, the consolidated financial statements). In our opinion, the consolidated financial statements present fairly, in all material respects, the financial position of the Partnership as of December 31, 2017 and 2016, and the results of its operations and its cash flows for each of the years in the three‑year period ended December 31, 2017, in conformity with U.S. generally accepted accounting principles.

We also have audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States) (PCAOB), the Partnership’s internal control over financial reporting as of December 31, 2017, based on criteria established in Internal Control - Integrated Framework (2013) issued by the Committee of Sponsoring Organizations of the Treadway Commission, and our report dated February 20, 2018 (not included herein) expressed an unqualified opinion on the effectiveness of the Company’s internal control over financial reporting.

Change in Accounting Principle

As discussed in Note 3 to the consolidated financial statements, the Partnership has changed its method of accounting for revenue recognition in 2017, 2016 and 2015 due to the adoption of ASU 2014-09, Revenue from Contracts with Customers (Topic 606), and subsequent amendments thereto.

Basis for Opinion

These consolidated financial statements are the responsibility of the Partnership’s management. Our responsibility is to express an opinion on these consolidated financial statements based on our audits. We are a public accounting firm registered with the PCAOB and are required to be independent with respect to the Partnership in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free of material misstatement, whether due to error or fraud. Our audits included performing procedures to assess the risks of material misstatement of the consolidated financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the consolidated financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements. We believe that our audits provide a reasonable basis for our opinion.

/s/ KPMG LLP

We have served as the Partnership’s auditor since 2014.

Houston, Texas

February 20, 2018, except as to Notes 12 and 20 which are as of June 15, 2018

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

(in millions, except unit data)

|

| | | | | | | | |

| | December 31, |

| | 2017 | | 2016 |

ASSETS | |

| | |

Current assets | | | | |

Cash and cash equivalents | | $ | — |

| | $ | — |

|

Restricted cash | | 1,589 |

| | 605 |

|

Accounts and other receivables | | 191 |

| | 90 |

|

Accounts receivable—affiliate | | 163 |

| | 99 |

|

Advances to affiliate | | 36 |

| | 38 |

|

Inventory | | 95 |

| | 97 |

|

Other current assets | | 65 |

| | 29 |

|

Total current assets | | 2,139 |

| | 958 |

|

| | | | |

Property, plant and equipment, net | | 15,139 |

| | 14,158 |

|

Debt issuance costs, net | | 38 |

| | 121 |

|

Non-current derivative assets | | 31 |

| | 83 |

|

Other non-current assets, net | | 206 |

| | 222 |

|

Total assets | | $ | 17,553 |

| | $ | 15,542 |

|

| | | | |

LIABILITIES AND PARTNERS’ EQUITY | | | | |

Current liabilities | | | | |

Accounts payable | | $ | 12 |

| | $ | 27 |

|

Accrued liabilities | | 637 |

| | 418 |

|

Current debt | | — |

| | 224 |

|

Due to affiliates | | 68 |

| | 99 |

|

Deferred revenue | | 111 |

| | 73 |

|

Deferred revenue—affiliate | | 1 |

| | 1 |

|

Derivative liabilities | | — |

| | 14 |

|

Total current liabilities | | 829 |

| | 856 |

|

| | | | |

Long-term debt, net | | 16,046 |

| | 14,209 |

|

Non-current deferred revenue | | 1 |

| | 5 |

|

Non-current derivative liabilities | | 3 |

| | 2 |

|

Other non-current liabilities | | 10 |

| | — |

|

Other non-current liabilities—affiliate | | 25 |

| | 27 |

|

| | | | |

Commitments and contingencies (see Note 16) | |

| |

|

| | | | |

Partners’ equity | | | | |

Common unitholders’ interest (348.6 million units and 57.1 million units issued and outstanding at December 31, 2017 and 2016, respectively) | | 1,670 |

| | 130 |

|

Class B unitholders’ interest (zero and 145.3 million units issued and outstanding at December 31, 2017 and 2016, respectively) | | — |

| | 62 |

|

Subordinated unitholders’ interest (135.4 million units issued and outstanding at December 31, 2017 and 2016) | | (1,043 | ) | | 240 |

|

General partner’s interest (2% interest with 9.9 million units and 6.9 million units issued and outstanding at December 31, 2017 and 2016, respectively) | | 12 |

| | 11 |

|

Total partners’ equity | | 639 |

|

| 443 |

|

Total liabilities and partners’ equity | | $ | 17,553 |

| | $ | 15,542 |

|

The accompanying notes are an integral part of these consolidated financial statements.

3

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS

(in millions, except per unit data)

|

| | | | | | | | | | | |

| Year Ended December 31, |

| 2017 | | 2016 | | 2015 |

Revenues | | | | | |

LNG revenues | $ | 2,635 |

| | $ | 539 |

| | $ | — |

|

LNG revenues—affiliate | 1,389 |

| | 294 |

| | — |

|

Regasification revenues | 260 |

| | 259 |

| | 259 |

|

Other revenues | 20 |

| | 4 |

| | 7 |

|

Other revenues—affiliate | — |

| | 4 |

| | 4 |

|

Total revenues | 4,304 |

| | 1,100 |

| | 270 |

|

| | | | | |

Operating costs and expenses | | | | | |

Cost (cost recovery) of sales (excluding depreciation and amortization expense shown separately below) | 2,320 |

| | 410 |

| | (31 | ) |

Cost of sales—affiliate | — |

| | 2 |

| | — |

|

Operating and maintenance expense | 292 |

| | 127 |

| | 62 |

|

Operating and maintenance expense—affiliate | 100 |

| | 52 |

| | 29 |

|

Development expense | 3 |

| | — |

| | 3 |

|

Development expense—affiliate | — |

| | — |

| | 1 |

|

General and administrative expense | 12 |

| | 13 |

| | 15 |

|

General and administrative expense—affiliate | 80 |

| | 90 |

| | 122 |

|

Depreciation and amortization expense | 339 |

| | 156 |

| | 66 |

|

Other | 2 |

| | — |

| | — |

|

Total operating costs and expenses | 3,148 |

| | 850 |

| | 267 |

|

| | | | | |

Income from operations | 1,156 |

| | 250 |

| | 3 |

|

| | | | | |

Other income (expense) | | | | | |

Interest expense, net of capitalized interest | (614 | ) | | (357 | ) | | (185 | ) |

Loss on early extinguishment of debt | (67 | ) | | (72 | ) | | (96 | ) |

Derivative gain (loss), net | 4 |

| | 6 |

| | (42 | ) |

Other income | 11 |

| | 2 |

| | 1 |

|

Total other expense | (666 | ) | | (421 | ) | | (322 | ) |

| | | | | |

Net income (loss) | $ | 490 |

| | $ | (171 | ) | | $ | (319 | ) |

| | | | | |

Basic and diluted net loss per common unit | $ | (1.32 | ) | | $ | (0.20 | ) | | $ | (0.43 | ) |

| | | | | |

Weighted average number of common units outstanding used for basic and diluted net loss per common unit calculation | 178.5 |

| | 57.1 |

| | 57.1 |

|

The accompanying notes are an integral part of these consolidated financial statements.

4

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF PARTNERS’ EQUITY

(in millions)

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Common Unitholders’ Interest | | Class B Unitholders’ Interest | | Subordinated Unitholder’s Interest | | General Partner’s Interest | | Total Partners’ Equity |

| Units | | Amount | | Units | | Amount | | Units | | Amount | | Units | | Amount | |

Balance at December 31, 2014 | 57.1 |

| | $ | 496 |

| | 145.3 |

| | $ | (38 | ) | | 135.4 |

| | $ | 648 |

| | 6.9 |

| | $ | 25 |

| | $ | 1,131 |

|

Net loss | — |

| | (93 | ) | | — |

| | — |

| | — |

| | (220 | ) | | — |

| | (6 | ) | | (319 | ) |

Distributions | — |

| | (97 | ) | | — |

| | — |

| | — |

| | — |

| | — |

| | (2 | ) | | (99 | ) |

Amortization of beneficial conversion feature of Class B units | — |

| | — |

| | — |

| | 1 |

| | — |

| | (1 | ) | | — |

| | — |

| | — |

|

Balance at December 31, 2015 | 57.1 |

| | 306 |

| | 145.3 |

| | (37 | ) | | 135.4 |

| | 427 |

| | 6.9 |

| | 17 |

| | 713 |

|

Net loss | — |

| | (50 | ) | | — |

| | — |

| | — |

| | (117 | ) | | — |

| | (4 | ) | | (171 | ) |

Distributions | — |

| | (97 | ) | | — |

| | — |

| | — |

| | — |

| | — |

| | (2 | ) | | (99 | ) |

Amortization of beneficial conversion feature of Class B units | — |

| | (29 | ) | | — |

| | 99 |

| | — |

| | (70 | ) | | — |

| | — |

| | — |

|

Balance at December 31, 2016 | 57.1 |

| | 130 |

| | 145.3 |

| | 62 |

| | 135.4 |

| | 240 |

| | 6.9 |

| | 11 |

| | 443 |

|

Net income | — |

| | 294 |

| | — |

| | — |

| | — |

| | 186 |

| | — |

| | 10 |

| | 490 |

|

Distributions | — |

| | (226 | ) | | — |

| | — |

| | — |

| | (59 | ) | | — |

| | (9 | ) | | (294 | ) |

Conversion of Class B units into common units | 291.5 |

| | 2,066 |

| | (145.3 | ) | | (2,066 | ) | | — |

| | — |

| | 3.0 |

| | — |

| | — |

|

Amortization of beneficial conversion feature of Class B units | — |

| | (594 | ) | | — |

| | 2,004 |

| | — |

| | (1,410 | ) | | — |

| | — |

| | — |

|

Balance at December 31, 2017 | 348.6 |

| | $ | 1,670 |

| | — |

| | $ | — |

| | 135.4 |

| | $ | (1,043 | ) | | 9.9 |

| | $ | 12 |

| | $ | 639 |

|

The accompanying notes are an integral part of these consolidated financial statements.

5

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS

(in millions)

|

| | | | | | | | | | | |

| Year Ended December 31, |

| 2017 | | 2016 | | 2015 |

Cash flows from operating activities | | | | | |

Net income (loss) | $ | 490 |

| | $ | (171 | ) | | $ | (319 | ) |

Adjustments to reconcile net income (loss) to net cash provided by (used in) operating activities: | | | | | |

Non-cash LNG inventory write-downs | — |

| | — |

| | 18 |

|

Depreciation and amortization expense | 339 |

| | 156 |

| | 66 |

|

Amortization of debt issuance costs, deferred commitment fees, premium and discount | 36 |

| | 30 |

| | 12 |

|

Loss on early extinguishment of debt | 67 |

| | 72 |

| | 96 |

|

Total losses (gains) on derivatives, net | 20 |

| | (48 | ) | | 7 |

|

Net cash used for settlement of derivative instruments | (16 | ) | | (8 | ) | | (41 | ) |

Other | 8 |

| | 1 |

| | — |

|

Changes in operating assets and liabilities: | | | | | |

Accounts and other receivables | (101 | ) | | (90 | ) | | — |

|

Accounts receivable—affiliate | (62 | ) | | (98 | ) | | 1 |

|

Advances to affiliate | (12 | ) | | — |

| | (13 | ) |

Inventory | 13 |

| | (58 | ) | | (25 | ) |

Accounts payable and accrued liabilities | 210 |

| | 167 |

| | (1 | ) |

Due to affiliates | (42 | ) | | 11 |

| | 15 |

|

Deferred revenue | 34 |

| | 42 |

| | (4 | ) |

Other, net | (5 | ) | | (7 | ) | | (11 | ) |

Other, net—affiliate | (2 | ) | | 1 |

| | 28 |

|

Net cash provided by (used in) operating activities | 977 |

| | — |

| | (171 | ) |

| | | | | |

Cash flows from investing activities | |

| | |

| | |

Property, plant and equipment, net | (1,290 | ) | | (2,315 | ) | | (2,913 | ) |

Other | — |

| | (38 | ) | | (62 | ) |

Net cash used in investing activities | (1,290 | ) | | (2,353 | ) | | (2,975 | ) |

| | | | | |

Cash flows from financing activities | |

| | |

| | |

Proceeds from issuances of debt | 3,814 |

| | 8,003 |

| | 2,860 |

|

Repayments of debt | (2,173 | ) | | (5,251 | ) | | — |

|

Debt issuance and deferred financing costs | (50 | ) | | (115 | ) | | (170 | ) |

Debt extinguishment costs | — |

| | (14 | ) | | — |

|

Distributions to owners | (294 | ) | | (99 | ) | | (99 | ) |

Net cash provided by financing activities | 1,297 |

| | 2,524 |

| | 2,591 |

|

| | | | | |

Net increase (decrease) in cash, cash equivalents and restricted cash | 984 |

| | 171 |

| | (555 | ) |

Cash, cash equivalents and restricted cash—beginning of period | 605 |

| | 434 |

| | 989 |

|

Cash, cash equivalents and restricted cash—end of period | $ | 1,589 |

| | $ | 605 |

| | $ | 434 |

|

Balances per Consolidated Balance Sheets:

|

| | | | | | | |

| December 31, |

| 2017 | | 2016 |

Cash and cash equivalents | $ | — |

| | $ | — |

|

Restricted cash | 1,589 |

| | 605 |

|

Total cash, cash equivalents and restricted cash | $ | 1,589 |

| | $ | 605 |

|

The accompanying notes are an integral part of these consolidated financial statements.

6

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

NOTE 1—ORGANIZATION AND NATURE OF OPERATIONS

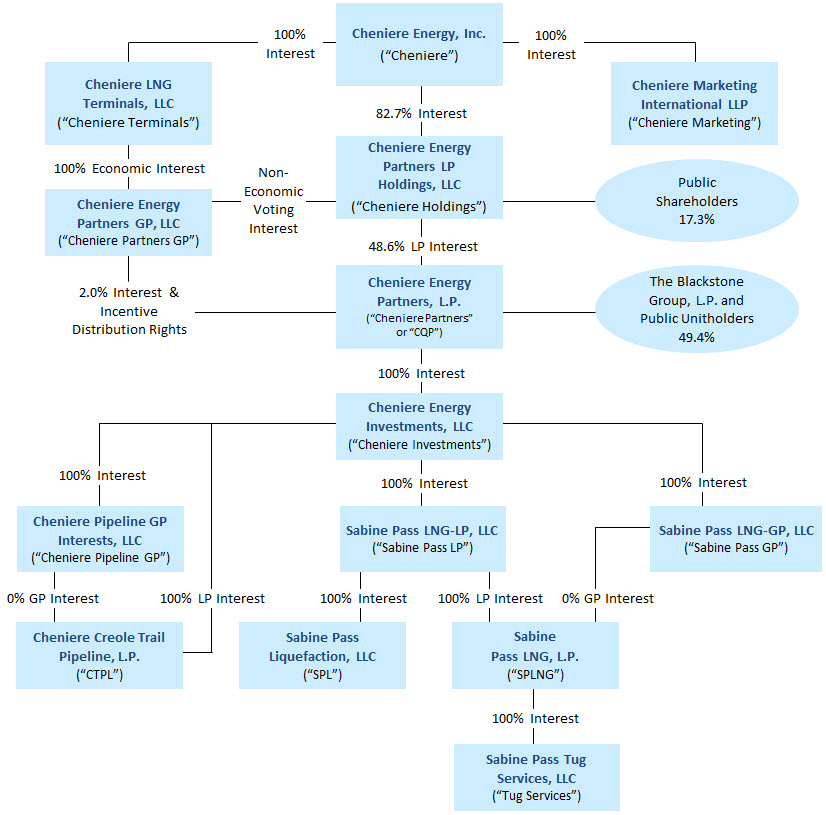

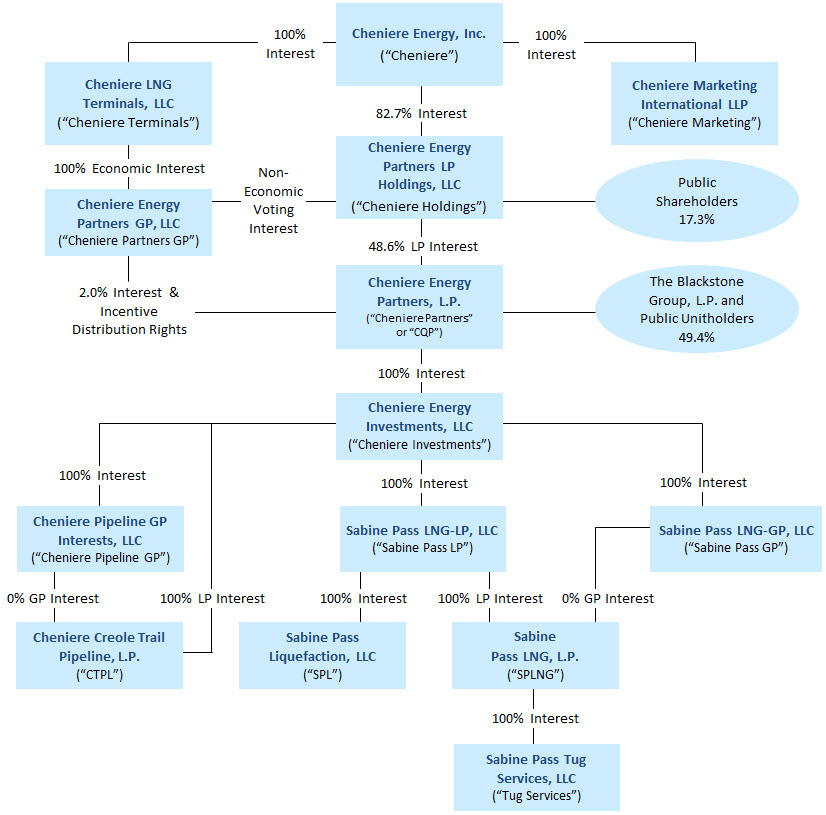

We are a publicly traded Delaware limited partnership (NYSE American: CQP) formed by Cheniere. Through SPL, we are developing, constructing and operating natural gas liquefaction facilities (the “Liquefaction Project”) at the Sabine Pass LNG terminal located in Cameron Parish, Louisiana, on the Sabine-Neches Waterway less than four miles from the Gulf Coast. We plan to construct up to six Trains, which are in various stages of development, construction and operations. Trains 1 through 4 are operational, Train 5 is under construction and Train 6 is being commercialized and has all necessary regulatory approvals in place. Each Train is expected to have a nominal production capacity, which is prior to adjusting for planned maintenance, production reliability and potential overdesign, of approximately 4.5 mtpa and an adjusted nominal production capacity of approximately 4.3 to 4.6 mtpa of LNG. Through our wholly owned subsidiary, SPLNG, we own and operate regasification facilities at the Sabine Pass LNG terminal, which includes pre-existing infrastructure of five LNG storage tanks with aggregate capacity of approximately 16.9 Bcfe, two marine berths that can each accommodate vessels with nominal capacity of up to 266,000 cubic meters and vaporizers with regasification capacity of approximately 4.0 Bcf/d. We also own a 94-mile pipeline that interconnects the Sabine Pass LNG terminal with a number of large interstate pipelines (the “Creole Trail Pipeline”) through CTPL.

As of December 31, 2017, Cheniere owned 100% of our general partner interest and 82.7% of Cheniere Holdings, which owned 104.5 million of our common units and 135.4 million of our subordinated units.

NOTE 2—UNITHOLDERS’ EQUITY

The common units and subordinated units represent limited partner interests in us. The holders of the units are entitled to participate in partnership distributions and exercise the rights and privileges available to limited partners under our partnership agreement. Our partnership agreement requires that, within 45 days after the end of each quarter, we distribute all of our available cash (as defined in our partnership agreement). Generally, our available cash is our cash on hand at the end of a quarter less the amount of any reserves established by our general partner. All distributions paid to date have been made from operating surplus as defined in the partnership agreement.

The holders of common units have the right to receive initial quarterly distributions of $0.425 per common unit, plus any arrearages thereon, before any distribution is made to the holders of the subordinated units. The holders of subordinated units will receive distributions only to the extent we have available cash above the initial quarterly distribution requirement for our common unitholders and general partner and certain reserves. Subordinated units will convert into common units on a one-for-one basis when we meet financial tests specified in the partnership agreement. Although common and subordinated unitholders are not obligated to fund losses of the Partnership, their capital accounts, which would be considered in allocating the net assets of the Partnership were it to be liquidated, continue to share in losses.

The general partner interest is entitled to at least 2% of all distributions made by us. In addition, the general partner holds incentive distribution rights (“IDRs”), which allow the general partner to receive a higher percentage of quarterly distributions of available cash from operating surplus after the initial quarterly distributions have been achieved and as additional target levels are met, but may transfer these rights separately from its general partner interest. The higher percentages range from 15% to 50%, inclusive of the general partner interest.

During 2012, Blackstone CQP Holdco and Cheniere completed their purchases of a new class of equity interests representing limited partner interests in us (“Class B units”) for total consideration of $1.5 billion and $500 million, respectively. Proceeds from the financings were used to fund a portion of the costs of developing, constructing and placing into service the first two Trains of the Liquefaction Project. In May 2013, Cheniere purchased an additional 12.0 million Class B units for consideration of $180 million in connection with our acquisition of CTPL and Cheniere Pipeline GP Interests, LLC. In 2013, Cheniere formed Cheniere Holdings to hold its limited partner interests in us. On a quarterly basis beginning on the date of the initial purchase date of the Class B units, the conversion value of the Class B units increased at a compounded rate of 3.5% per quarter.

On August 2, 2017, the 45.3 million Class B units held by Cheniere Holdings and 100.0 million Class B units held by Blackstone CQP Holdco mandatorily converted into our common units in accordance with the terms of our partnership agreement. Upon conversion of the Class B units, Cheniere Holdings, Blackstone CQP Holdco and the public owned a 48.6%, 40.3% and 9.1% interest in us, respectively. Cheniere Holdings’ ownership percentage includes its subordinated units and Blackstone CQP Holdco’s ownership percentage excludes any common units that may be deemed to be beneficially owned by Blackstone Group, an affiliate of Blackstone CQP Holdco.

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

NOTE 3—SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of Presentation

Our Consolidated Financial Statements have been prepared in accordance with GAAP. The Consolidated Financial Statements include the accounts of Cheniere Partners and its majority owned subsidiaries. All significant intercompany accounts and transactions have been eliminated in consolidation. Certain reclassifications have been made to conform prior period information to the current presentation. The reclassifications did not have a material effect on our consolidated financial position, results of operations or cash flows.

On January 1, 2018, we adopted ASU 2014-09, Revenue from Contracts with Customers (Topic 606), and subsequent amendments thereto (“ASC 606”) using the full retrospective method. We have elected to adopt the new accounting standard retrospectively and have recast the accompanying consolidated financial statements to reflect the adoption of ASC 606 for all periods presented. The adoption of ASC 606 did not impact our previously reported consolidated financial statements in any prior period nor did it result in a cumulative effect adjustment to retained earnings.

Use of Estimates

The preparation of Consolidated Financial Statements in conformity with GAAP requires management to make certain estimates and assumptions that affect the amounts reported in the Consolidated Financial Statements and the accompanying notes. Management evaluates its estimates and related assumptions regularly, including those related to the value of property, plant and equipment, derivative instruments, asset retirement obligations (“AROs”) and fair value measurements. Changes in facts and circumstances or additional information may result in revised estimates, and actual results may differ from these estimates.

Fair Value

Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants. Hierarchy Levels 1, 2 and 3 are terms for the priority of inputs to valuation approaches used to measure fair value. Hierarchy Level 1 inputs are quoted prices in active markets for identical assets or liabilities. Hierarchy Level 2 inputs are inputs other than quoted prices included within Level 1 that are directly or indirectly observable for the asset or liability. Hierarchy Level 3 inputs are inputs that are not observable in the market.

In determining fair value, we use observable market data when available, or models that incorporate observable market data. In addition to market information, we incorporate transaction-specific details that, in management’s judgment, market participants would take into account in measuring fair value. We maximize the use of observable inputs and minimize our use of unobservable inputs in arriving at fair value estimates.

Recurring fair-value measurements are performed for derivative instruments as disclosed in Note 8—Derivative Instruments. The carrying amount of cash and cash equivalents, restricted cash, accounts receivable and accounts payable reported on the Consolidated Balance Sheets approximates fair value. The fair value of debt is the estimated amount we would have to pay to repurchase our debt in the open market, including any premium or discount attributable to the difference between the stated interest rate and market interest rate at each balance sheet date. Debt fair values, as disclosed in Note 11—Debt, are based on quoted market prices for identical instruments, if available, or based on valuations of similar debt instruments using observable or unobservable inputs. Non-financial assets and liabilities initially measured at fair value include intangible assets and AROs.

Revenue Recognition

We recognize revenues when we transfer control of promised goods or services to our customers in an amount that reflects the consideration to which we expect to be entitled to in exchange for those goods or services. Revenues from the sale of LNG are recognized as LNG revenues. LNG regasification capacity payments are recognized as regasification revenues. We also recognize tug services fees, which were historically included in regasification revenues but are now included within other revenues on our Consolidated Statements of Operations, that are received by Sabine Pass Tug Services, LLC (“Tug Services”), a wholly owned subsidiary of SPLNG. See Note 12—Revenues from Contracts with Customers for further discussion of revenues.

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

Cash and Cash Equivalents

We consider all highly liquid investments with an original maturity of three months or less to be cash equivalents.

Restricted Cash

Restricted cash consists of funds that are contractually restricted as to usage or withdrawal and have been presented separately from cash and cash equivalents on our Consolidated Balance Sheets.

Accounts Receivable

Accounts receivable is reported net of allowances for doubtful accounts. Impaired receivables are specifically identified and evaluated for expected losses. The expected loss on impaired receivables is primarily determined based on the debtor’s ability to pay and the estimated value of any collateral. We did not recognize any bad debt expense related to accounts receivable during the years ended December 31, 2017, 2016 and 2015.

Inventory

LNG and natural gas inventory are recorded at the lower of weighted average cost and net realizable value. Materials and other inventory are recorded at the lower of cost and net realizable value and subsequently charged to expense when issued. During the year ended December 31, 2015, we recognized $18 million as operating and maintenance expense as a result of write-down for LNG inventory purchased to maintain the cryogenic readiness of the regasification facilities at the Sabine Pass LNG terminal. We did not recognize any operating and maintenance expense related to inventory write-downs during the years ended December 31, 2017 and 2016.

Accounting for LNG Activities

Generally, we begin capitalizing the costs of our LNG terminals and related pipelines once the individual project meets the following criteria: (1) regulatory approval has been received, (2) financing for the project is available and (3) management has committed to commence construction. Prior to meeting these criteria, most of the costs associated with a project are expensed as incurred. These costs primarily include professional fees associated with front-end engineering and design work, costs of securing necessary regulatory approvals and other preliminary investigation and development activities related to our LNG terminals and related pipelines.

Generally, costs that are capitalized prior to a project meeting the criteria otherwise necessary for capitalization include: land and lease option costs that are capitalized as property, plant and equipment and certain permits that are capitalized as other non-current assets. The costs of lease options are amortized over the life of the lease once obtained. If no lease is obtained, the costs are expensed.

We capitalize interest and other related debt costs during the construction period of our LNG terminal and related pipeline. Upon commencement of operations, capitalized interest, as a component of the total cost, is amortized over the estimated useful life of the asset.

Property, Plant and Equipment

Property, plant and equipment are recorded at cost. Expenditures for construction and commissioning activities, major renewals and betterments that extend the useful life of an asset are capitalized, while expenditures for maintenance and repairs (including those for planned major maintenance projects) to maintain property, plant and equipment in operating condition are generally expensed as incurred. Interest costs incurred on debt obtained for the construction of property, plant and equipment are capitalized as construction-in-process over the construction period or related debt term, whichever is shorter. We depreciate our property, plant and equipment using the straight-line depreciation method. Upon retirement or other disposition of property, plant and equipment, the cost and related accumulated depreciation are removed from the account, and the resulting gains or losses are recorded in other operating costs and expenses.

Management tests property, plant and equipment for impairment whenever events or changes in circumstances have indicated that the carrying amount of property, plant and equipment might not be recoverable. Assets are grouped at the lowest level for

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

which there are identifiable cash flows that are largely independent of the cash flows of other groups of assets for purposes of assessing recoverability. Recoverability generally is determined by comparing the carrying value of the asset to the expected undiscounted future cash flows of the asset. If the carrying value of the asset is not recoverable, the amount of impairment loss is measured as the excess, if any, of the carrying value of the asset over its estimated fair value. We did not record any impairments related to property, plant and equipment during the years ended December 31, 2017, 2016 and 2015, respectively.

Regulated Natural Gas Pipelines

The Creole Trail Pipeline is subject to the jurisdiction of the FERC in accordance with the Natural Gas Act of 1938 and the Natural Gas Policy Act of 1978. The economic effects of regulation can result in a regulated company recording as assets those costs that have been or are expected to be approved for recovery from customers, or recording as liabilities those amounts that are expected to be required to be returned to customers, in a rate-setting process in a period different from the period in which the amounts would be recorded by an unregulated enterprise. Accordingly, we record assets and liabilities that result from the regulated rate-making process that may not be recorded under GAAP for non-regulated entities. We continually assess whether regulatory assets are probable of future recovery by considering factors such as applicable regulatory changes and recent rate orders applicable to other regulated entities. Based on this continual assessment, we believe the existing regulatory assets are probable of recovery. These regulatory assets and liabilities are primarily classified in our Consolidated Balance Sheets as other assets and other liabilities. We periodically evaluate their applicability under GAAP and consider factors such as regulatory changes and the effect of competition. If cost-based regulation ends or competition increases, we may have to reduce our asset balances to reflect a market basis less than cost and write off the associated regulatory assets and liabilities.

Items that may influence our assessment are:

| |

• | inability to recover cost increases due to rate caps and rate case moratoriums; |

| |

• | inability to recover capitalized costs, including an adequate return on those costs through the rate-making process and the FERC proceedings; |

| |

• | increased competition and discounting in the markets we serve; and |

| |

• | impacts of ongoing regulatory initiatives in the natural gas industry. |

Natural gas pipeline costs include amounts capitalized as an Allowance for Funds Used During Construction (“AFUDC”). The rates used in the calculation of AFUDC are determined in accordance with guidelines established by the FERC. AFUDC represents the cost of debt and equity funds used to finance our natural gas pipeline additions during construction. AFUDC is capitalized as a part of the cost of our natural gas pipelines. Under regulatory rate practices, we generally are permitted to recover AFUDC, and a fair return thereon, through our rate base after our natural gas pipelines are placed in service.

Derivative Instruments

We use derivative instruments to hedge our exposure to cash flow variability from interest rate and commodity price risk. Derivative instruments are recorded at fair value and included in our Consolidated Balance Sheets as assets or liabilities depending on the derivative position and the expected timing of settlement, unless they satisfy criteria for and we elect the normal purchases and sales exception. When we have the contractual right and intend to net settle, derivative assets and liabilities are reported on a net basis.

Changes in the fair value of our derivative instruments are recorded in earnings, unless we elect to apply hedge accounting and meet specified criteria, including completing contemporaneous hedge documentation. We did not have any derivative instruments designated as cash flow hedges during the years ended December 31, 2017, 2016 and 2015. See Note 8—Derivative Instruments for additional details about our derivative instruments.

Concentration of Credit Risk

Financial instruments that potentially subject us to a concentration of credit risk consist principally of cash and cash equivalents and restricted cash. We maintain cash balances at financial institutions, which may at times be in excess of federally insured levels. We have not incurred losses related to these balances to date.

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

The use of derivative instruments exposes us to counterparty credit risk, or the risk that a counterparty will be unable to meet its commitments. Our interest rate derivative instruments are placed with investment grade financial institutions whom we believe are acceptable credit risks. Certain of our commodity derivative transactions are executed through over-the-counter contracts which are subject to nominal credit risk as these transactions are settled on a daily margin basis with investment grade financial institutions. Collateral deposited for such contracts is recorded as other current asset. We monitor counterparty creditworthiness on an ongoing basis; however, we cannot predict sudden changes in counterparties’ creditworthiness. In addition, even if such changes are not sudden, we may be limited in our ability to mitigate an increase in counterparty credit risk. Should one of these counterparties not perform, we may not realize the benefit of some of our derivative instruments.

SPL has entered into six fixed price SPAs with terms of at least 20 years with six unaffiliated third parties. SPL is dependent on the respective customers’ creditworthiness and their willingness to perform under their respective SPAs. See Note 17—Customer Concentration for additional details about our customer concentration.

SPLNG has entered into two long-term TUAs with unaffiliated third parties for regasification capacity at the Sabine Pass LNG terminal. SPLNG is dependent on the respective customers’ creditworthiness and their willingness to perform under their respective TUAs. SPLNG has mitigated this credit risk by securing TUAs for a significant portion of its regasification capacity with creditworthy third-party customers with a minimum Standard & Poor’s rating of A.

Debt

Our debt consists of current and long-term secured debt securities and credit facilities with banks and other lenders. Debt issuances are placed directly by us or through securities dealers or underwriters and are held by institutional and retail investors.

Debt is recorded on our Consolidated Balance Sheets at par value adjusted for unamortized discount or premium and net of unamortized debt issuance costs related to term notes. Discounts, premiums and debt issuance costs directly related to the issuance of debt are amortized over the life of the debt and are recorded in interest expense, net of capitalized interest using the effective interest method. Gains and losses on the extinguishment of debt are recorded in gains and losses on the extinguishment of debt on our Consolidated Statements of Operations.

Debt issuance costs consist primarily of arrangement fees, professional fees, legal fees and printing costs. These costs are recorded as a direct deduction from the debt liability unless incurred in connection with a line of credit arrangement, in which case they are presented as an asset on our Consolidated Balance Sheet. Debt issuance costs are amortized to interest expense or property, plant and equipment over the term of the related debt facility. Upon early retirement of debt or amendment to a debt agreement, certain fees are written off to loss on early extinguishment of debt.

Asset Retirement Obligations

We recognize AROs for legal obligations associated with the retirement of long-lived assets that result from the acquisition, construction, development and/or normal use of the asset and for conditional AROs in which the timing or method of settlement are conditional on a future event that may or may not be within our control. The fair value of a liability for an ARO is recognized in the period in which it is incurred, if a reasonable estimate of fair value can be made. The fair value of the liability is added to the carrying amount of the associated asset. This additional carrying amount is depreciated over the estimated useful life of the asset. Our assessment of AROs is described below.

We have not recorded an ARO associated with the Sabine Pass LNG terminal. Based on the real property lease agreements at the Sabine Pass LNG terminal, at the expiration of the term of the leases we are required to surrender the LNG terminal in good working order and repair, with normal wear and tear and casualty expected. Our property lease agreements at the Sabine Pass LNG terminal have terms of up to 90 years including renewal options. We have determined that the cost to surrender the Sabine Pass LNG terminal in good order and repair, with normal wear and tear and casualty expected, is immaterial.

We have not recorded an ARO associated with the Creole Trail Pipeline. We believe that it is not feasible to predict when the natural gas transportation services provided by the Creole Trail Pipeline will no longer be utilized. In addition, our right-of-way agreements associated with the Creole Trail Pipeline have no stipulated termination dates. We intend to operate the Creole Trail Pipeline as long as supply and demand for natural gas exists in the United States and intend to maintain it regularly.

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

Income Taxes

We are not subject to federal or state income taxes, as our partners are taxed individually on their allocable share of our taxable income. At December 31, 2017, the tax basis of our assets and liabilities was $3.1 billion less than the reported amounts of our assets and liabilities. See Note 13—Related Party Transactions for details about income taxes under our tax sharing agreements.

Business Segment

Our liquefaction and regasification operations at the Sabine Pass LNG terminal represent a single reportable segment. Our chief operating decision maker reviews the financial results of Cheniere Partners in total when evaluating financial performance and for purposes of allocating resources.

NOTE 4—RESTRICTED CASH

Restricted cash consists of funds that are contractually restricted as to usage or withdrawal and have been presented separately from cash and cash equivalents on our Consolidated Balance Sheets. As of December 31, 2017 and 2016, restricted cash consisted of the following (in millions):

|

| | | | | | | | |

| | December 31, |

| | 2017 | | 2016 |

Current restricted cash | | | | |

Liquefaction Project | | $ | 544 |

| | $ | 358 |

|

CQP and cash held by guarantor subsidiaries | | 1,045 |

| | 247 |

|

Total current restricted cash | | $ | 1,589 |

| | $ | 605 |

|

NOTE 5—ACCOUNTS AND OTHER RECEIVABLES

As of December 31, 2017 and 2016, accounts and other receivables consisted of the following (in millions):

|

| | | | | | | | |

| | December 31, |

| | 2017 | | 2016 |

SPL trade receivable | | $ | 185 |

| | $ | 88 |

|

Other accounts receivable | | 6 |

| | 2 |

|

Total accounts and other receivables | | $ | 191 |

| | $ | 90 |

|

Pursuant to the accounts agreement entered into with the collateral trustee for the benefit of SPL’s debt holders, SPL is required to deposit all cash received into reserve accounts controlled by the collateral trustee. The usage or withdrawal of such cash is restricted to the payment of liabilities related to the Liquefaction Project and other restricted payments.

NOTE 6—INVENTORY

As of December 31, 2017 and 2016, inventory consisted of the following (in millions):

|

| | | | | | | | |

| | December 31, |

| | 2017 | | 2016 |

Natural gas | | $ | 17 |

| | $ | 15 |

|

LNG | | 26 |

| | 45 |

|

Materials and other | | 52 |

| | 37 |

|

Total inventory | | $ | 95 |

| | $ | 97 |

|

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

NOTE 7—PROPERTY, PLANT AND EQUIPMENT

Property, plant and equipment, net consists of LNG terminal costs and fixed assets, as follows (in millions):

|

| | | | | | | | |

| | December 31, |

| | 2017 | | 2016 |

LNG terminal costs | | | | |

LNG terminal | | $ | 12,703 |

| | $ | 7,976 |

|

LNG terminal construction-in-process | | 3,310 |

| | 6,728 |

|

Accumulated depreciation | | (880 | ) | | (553 | ) |

Total LNG terminal costs, net | | 15,133 |

| | 14,151 |

|

Fixed assets | | |

| | |

|

Fixed assets | | 23 |

| | 20 |

|

Accumulated depreciation | | (17 | ) | | (13 | ) |

Total fixed assets, net | | 6 |

| | 7 |

|

Property, plant and equipment, net | | $ | 15,139 |

| | $ | 14,158 |

|

Depreciation expense was $331 million, $148 million and $65 million in the years ended December 31, 2017, 2016 and 2015, respectively.

We realized offsets to LNG terminal costs of $301 million and $201 million in the years ended December 31, 2017 and 2016, respectively, that were related to the sale of commissioning cargoes because these amounts were earned or loaded prior to the start of commercial operations of the respective Train of the Liquefaction Project, during the testing phase for its construction.

LNG Terminal Costs

The Sabine Pass LNG terminal is depreciated using the straight-line depreciation method applied to groups of LNG terminal assets with varying useful lives. The identifiable components of the Sabine Pass LNG terminal with similar estimated useful lives have a depreciable range between 6 and 50 years, as follows:

|

| | |

Components | | Useful life (yrs) |

LNG storage tanks | | 50 |

Natural gas pipeline facilities | | 40 |

Marine berth, electrical, facility and roads | | 35 |

Regasification processing equipment | | 30 |

Sendout pumps | | 20 |

Liquefaction processing equipment | | 6-50 |

Other | | 15-30 |

Fixed Assets and Other

Our fixed assets and other are recorded at cost and are depreciated on a straight-line method based on estimated lives of the individual assets or groups of assets.

NOTE 8—DERIVATIVE INSTRUMENTS

We have entered into the following derivative instruments that are reported at fair value:

| |

• | interest rate swaps to hedge the exposure to volatility in a portion of the floating-rate interest payments under certain credit facilities (“Interest Rate Derivatives”) and |

| |

• | commodity derivatives consisting of natural gas supply contracts for the commissioning and operation of the Liquefaction Project (“Physical Liquefaction Supply Derivatives”) and associated economic hedges (“Financial Liquefaction Supply Derivatives,” and collectively with the Physical Liquefaction Supply Derivatives, the “Liquefaction Supply Derivatives”). |

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

We recognize our derivative instruments as either assets or liabilities and measure those instruments at fair value. None of our derivative instruments are designated as cash flow hedging instruments, and changes in fair value are recorded within our Consolidated Statements of Operations to the extent not utilized for the commissioning process.

The following table shows the fair value of our derivative instruments that are required to be measured at fair value on a recurring basis as of December 31, 2017 and 2016, which are classified as other current assets, non-current derivative assets, derivative liabilities or non-current derivative liabilities in our Consolidated Balance Sheets (in millions).

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Fair Value Measurements as of |

| December 31, 2017 | | December 31, 2016 |

| Quoted Prices in Active Markets (Level 1) | | Significant Other Observable Inputs (Level 2) | | Significant Unobservable Inputs (Level 3) | | Total | | Quoted Prices in Active Markets (Level 1) | | Significant Other Observable Inputs (Level 2) | | Significant Unobservable Inputs (Level 3) | | Total |

SPL Interest Rate Derivatives liability | $ | — |

| | $ | — |

| | $ | — |

| | $ | — |

| | $ | — |

| | $ | (6 | ) | | $ | — |

| | $ | (6 | ) |

CQP Interest Rate Derivatives asset | — |

| | 21 |

| | — |

| | 21 |

| | — |

| | 13 |

| | — |

| | 13 |

|

Liquefaction Supply Derivatives asset (liability) | 2 |

| | 10 |

| | 43 |

| | 55 |

| | (4 | ) | | (2 | ) | | 79 |

| | 73 |

|

We value our Interest Rate Derivatives using an income-based approach, utilizing observable inputs to the valuation model including interest rate curves, risk adjusted discount rates, credit spreads and other relevant data. We value our Liquefaction Supply Derivatives using market based approach incorporating present value techniques, as needed, using observable commodity price curves, when available, and other relevant data.

The fair value of our Physical Liquefaction Supply Derivatives is predominantly driven by market commodity basis prices and our assessment of the associated conditions precedent, including evaluating whether the respective market is available as pipeline infrastructure is developed. Upon the satisfaction of conditions precedent, including completion and placement into service of relevant pipeline infrastructure to accommodate marketable physical gas flow, we recognize a gain or loss based on the fair value of the respective natural gas supply contracts.

We include a portion of our Physical Liquefaction Supply Derivatives as Level 3 within the valuation hierarchy as the fair value is developed through the use of internal models which may be impacted by inputs that are unobservable in the marketplace. The curves used to generate the fair value of our Physical Liquefaction Supply Derivatives are based on basis adjustments applied to forward curves for a liquid trading point. In addition, there may be observable liquid market basis information in the near term, but terms of a Physical Liquefaction Supply Derivatives contract may exceed the period for which such information is available, resulting in a Level 3 classification. In these instances, the fair value of the contract incorporates extrapolation assumptions made in the determination of the market basis price for future delivery periods in which applicable commodity basis prices were either not observable or lacked corroborative market data.

The Level 3 fair value measurements of our Physical Liquefaction Supply Derivatives could be materially impacted by a significant change in certain natural gas market basis spreads due to the contractual notional amount represented by our Level 3 positions, which is a substantial portion of our overall Physical Liquefaction Supply portfolio. The following table includes quantitative information for the unobservable inputs for our Level 3 Physical Liquefaction Supply Derivatives as of December 31, 2017:

|

| | | | | | | | |

| | Net Fair Value Asset (in millions) | | Valuation Approach | | Significant Unobservable Input | | Significant Unobservable Inputs Range |

Physical Liquefaction Supply Derivatives | | $43 | | Market approach incorporating present value techniques | | Basis Spread | | $(0.503) - $0.432 |

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

The following table shows the changes in the fair value of our Level 3 Physical Liquefaction Supply Derivatives during the years ended December 31, 2017, 2016 and 2015 (in millions):

|

| | | | | | | | | | | | |

| | Year Ended December 31, |

| | 2017 | | 2016 | | 2015 |

Balance, beginning of period | | $ | 79 |

| | $ | 32 |

| | $ | — |

|

Realized and mark-to-market gains (losses): | | | | | | |

Included in cost of sales (1) | | (37 | ) | | 48 |

| | 32 |

|

Purchases and settlements: | | | | | | |

Purchases | | 14 |

| | 1 |

| | — |

|

Settlements (1) | | (12 | ) | | (2 | ) | | — |

|

Transfers out of Level 3 | | (1 | ) | | — |

| | — |

|

Balance, end of period | | $ | 43 |

| | $ | 79 |

| | $ | 32 |

|

Change in unrealized gains relating to instruments still held at end of period | | $ | (37 | ) | | $ | 49 |

| | $ | 32 |

|

| |

(1) | Does not include the decrease in fair value of $1 million related to the realized gains capitalized during the year ended December 31, 2016. |

Derivative assets and liabilities arising from our derivative contracts with the same counterparty are reported on a net basis, as all counterparty derivative contracts provide for net settlement. The use of derivative instruments exposes us to counterparty credit risk, or the risk that a counterparty will be unable to meet its commitments in instances when our derivative instruments are in an asset position. Additionally, we evaluate our own ability to meet our commitments in instances where our derivative instruments are in a liability position. Our derivative instruments are subject to contractual provisions which provide for the unconditional right of set-off for all derivative assets and liabilities with a given counterparty in the event of default.

Interest Rate Derivatives

SPL had entered into interest rate swaps (“SPL Interest Rate Derivatives”) to protect against volatility of future cash flows and hedge a portion of the variable interest payments on the credit facilities it entered into in June 2015 (the “2015 SPL Credit Facilities”), based on a portion of the expected outstanding borrowings over the term of the 2015 SPL Credit Facilities. In March 2017, SPL settled the SPL Interest Rate Derivatives and recognized a derivative loss of $7 million in conjunction with the termination of approximately $1.6 billion of commitments under the 2015 SPL Credit Facilities, as discussed in Note 11—Debt.

We have entered into interest rate swaps (“CQP Interest Rate Derivatives”) to protect against volatility of future cash flows and hedge a portion of the variable interest payments on our $2.8 billion credit facilities (the “2016 CQP Credit Facilities”), based on a portion of the expected outstanding borrowings over the term of the 2016 CQP Credit Facilities.

As of December 31, 2017, we had the following Interest Rate Derivatives outstanding:

|

| | | | | | | | | | | | |

| | Initial Notional Amount | | Maximum Notional Amount | | Effective Date | | Maturity Date | | Weighted Average Fixed Interest Rate Paid | | Variable Interest Rate Received |

CQP Interest Rate Derivatives | | $225 million | | $1.3 billion | | March 22, 2016 | | February 29, 2020 | | 1.19% | | One-month LIBOR |

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

The following table shows the fair value and location of our Interest Rate Derivatives on our Consolidated Balance Sheets (in millions):

|

| | | | | | | | | | | | | | | | | | | | | | | | |

| | December 31, 2017 | | December 31, 2016 |

| | SPL Interest Rate Derivatives | | CQP Interest Rate Derivatives | | Total | | SPL Interest Rate Derivatives | | CQP Interest Rate Derivatives | | Total |

Balance Sheet Location | | | | | | | | | | | | |

Other current assets | | $ | — |

| | $ | 7 |

| | $ | 7 |

| | $ | — |

| | $ | — |

| | $ | — |

|

Non-current derivative assets | | — |

| | 14 |

| | 14 |

| | — |

| | 16 |

| | 16 |

|

Total derivative assets | | — |

| | 21 |

| | 21 |

| | — |

| | 16 |

| | 16 |

|

| | | | | | | | | | | | |

Derivative liabilities | | — |

| | — |

| | — |

| | (4 | ) | | (3 | ) | | (7 | ) |

Non-current derivative liabilities | | — |

| | — |

| | — |

| | (2 | ) | | — |

| | (2 | ) |

Total derivative liabilities | | — |

| | — |

| | — |

| | (6 | ) | | (3 | ) | | (9 | ) |

| | | | | | | | | | | | |

Derivative asset (liability), net | | $ | — |

| | $ | 21 |

| | $ | 21 |

| | $ | (6 | ) | | $ | 13 |

| | $ | 7 |

|

The following table shows the changes in the fair value and settlements of our Interest Rate Derivatives recorded in derivative gain (loss), net on our Consolidated Statements of Operations during the years ended December 31, 2017, 2016 and 2015 (in millions):

|

| | | | | | | | | | | | |

| | Year Ended December 31, |

| | 2017 | | 2016 | | 2015 |

SPL Interest Rate Derivatives loss | | $ | (2 | ) | | $ | (6 | ) | | $ | (42 | ) |

CQP Interest Rate Derivatives gain | | 6 |

| | 12 |

| | — |

|

Liquefaction Supply Derivatives

SPL has entered into index-based physical natural gas supply contracts and associated economic hedges, if applicable, to purchase natural gas for the commissioning and operation of the Liquefaction Project. The terms of the noncurrent physical natural gas supply contracts range from approximately one to seven years, most of which commence upon the satisfaction of certain conditions precedent, if not already met, such as the date of first commercial delivery of specified Trains of the Liquefaction Project.

Our Financial Liquefaction Supply Derivatives are executed through over-the-counter contracts which are subject to nominal credit risk as these transactions are settled on a daily margin basis with investment grade financial institutions. We are required by these financial institutions to use margin deposits as credit support for our Financial Liquefaction Supply Derivatives activities.

SPL had secured up to approximately 2,214 TBtu and 1,994 TBtu of natural gas feedstock through natural gas supply contracts as of December 31, 2017 and 2016, respectively. The notional natural gas position of our Liquefaction Supply Derivatives was approximately 1,520 TBtu and 1,117 TBtu as of December 31, 2017 and 2016, respectively.

The following table shows the fair value and location of our Liquefaction Supply Derivatives on our Consolidated Balance Sheets (in millions):

|

| | | | | | | | | |

| | | Fair Value Measurements as of (1) |

| Balance Sheet Location | | December 31, 2017 | | December 31, 2016 |

Liquefaction Supply Derivatives | Other current assets | | $ | 41 |

| | $ | 13 |

|

Liquefaction Supply Derivatives | Non-current derivative assets | | 17 |

| | 67 |

|

Liquefaction Supply Derivatives | Derivative liabilities | | — |

| | (7 | ) |

Liquefaction Supply Derivatives | Non-current derivative liabilities | | (3 | ) | | — |

|

| |

(1) | Does not include a collateral call of $1 million and a collateral deposit of $6 million for such contracts, which are included in other current assets in our Consolidated Balance Sheets as of December 31, 2017 and 2016, respectively. |

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

The following table shows the changes in the fair value, settlements and location of our Liquefaction Supply Derivatives recorded on our Consolidated Statements of Operations during the years ended December 31, 2017, 2016 and 2015 (in millions):

|

| | | | | | | | | | | | | |

| | | Year Ended December 31, |

| Statement of Operations Location (1) | | 2017 | | 2016 | | 2015 |

Liquefaction Supply Derivatives loss (gain) (2) | Cost of sales | | $ | 24 |

| | $ | (42 | ) | | $ | (33 | ) |

| |

(1) | Fair value fluctuations associated with commodity derivative activities are classified and presented consistently with the item economically hedged and the nature and intent of the derivative instrument. |

| |

(2) | Does not include the realized value associated with derivative instruments that settle through physical delivery. |

Consolidated Balance Sheet Presentation

Our derivative instruments are presented on a net basis on our Consolidated Balance Sheets as described above. The following table shows the fair value of our derivatives outstanding on a gross and net basis (in millions):

|

| | | | | | | | | | | | |

| | Gross Amounts Recognized | | Gross Amounts Offset in the Consolidated Balance Sheets | | Net Amounts Presented in the Consolidated Balance Sheets |

Offsetting Derivative Assets (Liabilities) | | | |

As of December 31, 2017 | | | | | | |

CQP Interest Rate Derivatives | | $ | 21 |

| | $ | — |

| | $ | 21 |

|

Liquefaction Supply Derivatives | | 64 |

| | (6 | ) | | 58 |

|

Liquefaction Supply Derivatives | | (3 | ) | | — |

| | (3 | ) |

As of December 31, 2016 | | | | | | |

SPL Interest Rate Derivatives | | $ | (6 | ) | | $ | — |

| | $ | (6 | ) |

CQP Interest Rate Derivatives | | 16 |

| | — |

| | 16 |

|

CQP Interest Rate Derivatives | | (3 | ) | | — |

| | (3 | ) |

Liquefaction Supply Derivatives | | 82 |

| | (2 | ) | | 80 |

|

Liquefaction Supply Derivatives | | (11 | ) | | 4 |

| | (7 | ) |

NOTE 9—OTHER NON-CURRENT ASSETS

As of December 31, 2017 and 2016, other non-current assets, net consisted of the following (in millions):

|

| | | | | | | | |

| | December 31, |

| | 2017 | | 2016 |

Advances made under EPC and non-EPC contracts | | $ | 26 |

| | $ | 23 |

|

Advances made to municipalities for water system enhancements | | 93 |

| | 95 |

|

Advances and other asset conveyances to third parties to support LNG terminals | | 30 |

| | 31 |

|

Tax-related payments and receivables | | 25 |

| | 28 |

|

Information technology service assets | | 24 |

| | 27 |

|

Other | | 8 |

| | 18 |

|

Total other non-current assets, net | | $ | 206 |

| | $ | 222 |

|

NOTE 10—ACCRUED LIABILITIES

As of December 31, 2017 and 2016, accrued liabilities consisted of the following (in millions):

|

| | | | | | | | |

| | December 31, |

| | 2017 | | 2016 |

Interest costs and related debt fees | | $ | 253 |

| | $ | 205 |

|

Sabine Pass LNG terminal and related pipeline costs | | 384 |

| | 211 |

|

Other accrued liabilities | | — |

| | 2 |

|

Total accrued liabilities | | $ | 637 |

| | $ | 418 |

|

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

NOTE 11—DEBT

As of December 31, 2017 and 2016, our debt consisted of the following (in millions):

|

| | | | | | | | |

| | December 31, |

| | 2017 | | 2016 |

Long-term debt: | | | | |

SPL | | | | |

5.625% Senior Secured Notes due 2021 (“2021 SPL Senior Notes”), net of unamortized premium of $6 and $7 | | $ | 2,006 |

| | $ | 2,007 |

|

6.25% Senior Secured Notes due 2022 (“2022 SPL Senior Notes”) | | 1,000 |

| | 1,000 |

|

5.625% Senior Secured Notes due 2023 (“2023 SPL Senior Notes”), net of unamortized premium of $5 and $6 | | 1,505 |

| | 1,506 |

|

5.75% Senior Secured Notes due 2024 (“2024 SPL Senior Notes”) | | 2,000 |

| | 2,000 |

|

5.625% Senior Secured Notes due 2025 (“2025 SPL Senior Notes”) | | 2,000 |

| | 2,000 |

|

5.875% Senior Secured Notes due 2026 (“2026 SPL Senior Notes”) | | 1,500 |

| | 1,500 |

|

5.00% Senior Secured Notes due 2027 (“2027 SPL Senior Notes”) | | 1,500 |

| | 1,500 |

|

4.200% Senior Secured Notes due 2028 (“2028 SPL Senior Notes”), net of unamortized discount of $1 and zero | | 1,349 |

| | — |

|

5.00% Senior Secured Notes due 2037 (“2037 SPL Senior Notes”) | | 800 |

| | — |

|

2015 SPL Credit Facilities | | — |

| | 314 |

|

Cheniere Partners | | | | |

5.250% Senior Notes due 2025 (“2025 CQP Senior Notes”) | | 1,500 |

| | — |

|

2016 CQP Credit Facilities | | 1,090 |

| | 2,560 |

|

Unamortized debt issuance costs | | (204 | ) | | (178 | ) |

Total long-term debt, net | | 16,046 |

| | 14,209 |

|

| | | | |

Current debt: | | | | |

$1.2 billion SPL Working Capital Facility (“SPL Working Capital Facility”) | | — |

| | 224 |

|

| | | | |

Total debt, net | | $ | 16,046 |

| | $ | 14,433 |

|

Below is a schedule of future principal payments that we are obligated to make, based on current construction schedules, on our outstanding debt at December 31, 2017 (in millions):

|

| | | | |

Years Ending December 31, | | Principal Payments |

2018 | | $ | — |

|

2019 | | 55 |

|

2020 | | 1,035 |

|

2021 | | 2,000 |

|

2022 | | 1,000 |

|

Thereafter | | 12,150 |

|

Total | | $ | 16,240 |

|

Senior Notes

SPL Senior Notes

In February 2017, SPL issued an aggregate principal amount of $800 million of the 2037 SPL Senior Notes on a private placement basis in reliance on the exemption from registration provided for under Section 4(a)(2) of the Securities Act of 1933, as amended. In March 2017, SPL issued an aggregate principal amount of $1.35 billion, before discount, of the 2028 SPL Senior Notes. Net proceeds of the offerings of the 2037 SPL Senior Notes and the 2028 SPL Senior Notes were $789 million and $1.33 billion, respectively, after deducting the initial purchasers’ commissions (for the 2028 SPL Senior Notes) and estimated fees and expenses. The net proceeds of the 2037 SPL Senior Notes, after provisioning for incremental interest required during construction, were used to prepay the then outstanding borrowings of $369 million under the 2015 SPL Credit Facilities and, along with the net proceeds of the 2028 SPL Senior Notes, the remainder is being used to pay a portion of the capital costs in connection with the

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

construction of Trains 1 through 5 of the Liquefaction Project in lieu of the terminated portion of the commitments under the 2015 SPL Credit Facilities.

In connection with the issuance of the 2037 SPL Senior Notes and the 2028 SPL Senior Notes, SPL terminated the remaining available balance of $1.6 billion under the 2015 SPL Credit Facilities, resulting in a write-off of debt issuance costs associated with the 2015 SPL Credit Facilities of $42 million during the year ended December 31, 2017.

The terms of the 2021 SPL Senior Notes, 2022 SPL Senior Notes, 2023 SPL Senior Notes, 2024 SPL Senior Notes, 2025 SPL Senior Notes, 2026 SPL Senior Notes, 2027 SPL Senior Notes and 2028 SPL Senior Notes (collectively with the 2037 SPL Senior Notes, the “SPL Senior Notes”) are governed by a common indenture (the “SPL Indenture”) and the terms of the 2037 SPL Senior Notes are governed by a separate indenture (the “2037 SPL Senior Notes Indenture”). Both the SPL Indenture and the 2037 SPL Senior Notes Indenture contain customary terms and events of default and certain covenants that, among other things, limit SPL’s ability and the ability of SPL’s restricted subsidiaries to incur additional indebtedness or issue preferred stock, make certain investments or pay dividends or distributions on capital stock or subordinated indebtedness or purchase, redeem or retire capital stock, sell or transfer assets, including capital stock of SPL’s restricted subsidiaries, restrict dividends or other payments by restricted subsidiaries, incur liens, enter into transactions with affiliates, dissolve, liquidate, consolidate, merge, sell or lease all or substantially all of SPL’s assets and enter into certain LNG sales contracts. Subject to permitted liens, the SPL Senior Notes are secured on a pari passu first-priority basis by a security interest in all of the membership interests in SPL and substantially all of SPL’s assets. SPL may not make any distributions until, among other requirements, deposits are made into debt service reserve accounts as required and a debt service coverage ratio test of 1.25:1.00 is satisfied. Semi-annual principal payments for the 2037 SPL Senior Notes are due on March 15 and September 15 of each year beginning September 15, 2025. Interest on the SPL Senior Notes is payable semi-annually in arrears.

At any time prior to three months before the respective dates of maturity for each series of the SPL Senior Notes (except for the 2026 SPL Senior Notes, 2027 SPL Senior Notes, 2028 SPL Senior Notes and 2037 SPL Senior Notes, in which case the time period is six months before the respective dates of maturity), SPL may redeem all or part of such series of the SPL Senior Notes at a redemption price equal to the “make-whole” price (except for the 2037 SPL Senior Notes, in which case the redemption price is equal to the “optional redemption” price) set forth in the respective indentures governing the SPL Senior Notes, plus accrued and unpaid interest, if any, to the date of redemption. SPL may also, at any time within three months of the respective maturity dates for each series of the SPL Senior Notes (except for the 2026 SPL Senior Notes, 2027 SPL Senior Notes, 2028 SPL Senior Notes and 2037 SPL Senior Notes, in which case the time period is within six months of the respective dates of maturity), redeem all or part of such series of the SPL Senior Notes at a redemption price equal to 100% of the principal amount of such series of the SPL Senior Notes to be redeemed, plus accrued and unpaid interest, if any, to the date of redemption.

2025 CQP Senior Notes

In September 2017, we issued an aggregate principal amount of $1.5 billion of the 2025 CQP Senior Notes, which are jointly and severally guaranteed by each of our subsidiaries other than SPL and, subject to certain conditions governing the release of its guarantee, Sabine Pass LNG-LP, LLC (collectively, the “CQP Guarantors”). Net proceeds of the offering of approximately $1.5 billion, after deducting the initial purchasers’ commissions and estimated fees and expenses, were used to prepay a portion of the outstanding indebtedness under the 2016 CQP Credit Facilities, resulting in a write-off of debt issuance costs associated with the 2016 CQP Credit Facilities of $25 million during the year ended December 31, 2017.

Borrowings under the 2025 CQP Senior Notes accrue interest at a fixed rate of 5.250%, and interest on the 2025 CQP Senior Notes is payable semi-annually in arrears. The 2025 CQP Senior Notes are governed by an indenture (the “CQP Indenture”), which contains customary terms and events of default and certain covenants that, among other things, limit our ability and the ability of the CQP Guarantors to incur liens and sell assets, enter into transactions with affiliates, enter into sale-leaseback transactions and consolidate, merge or sell, lease or otherwise dispose of all or substantially all of the applicable entity’s properties or assets.

At any time prior to October 1, 2020, we may redeem all or a part of the 2025 CQP Senior Notes at a redemption price equal to 100% of the aggregate principal amount of the 2025 CQP Senior Notes redeemed, plus the “applicable premium” set forth in the CQP Indenture, plus accrued and unpaid interest, if any, to the date of redemption. In addition, at any time prior to October 1, 2020, we may redeem up to 35% of the aggregate principal amount of the 2025 CQP Senior Notes with an amount of cash not greater than the net cash proceeds from certain equity offerings at a redemption price equal to 105.250% of the aggregate principal amount of the 2025 CQP Senior Notes redeemed, plus accrued and unpaid interest, if any, to the date of redemption. We also may

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

at any time on or after October 1, 2020 through the maturity date of October 1, 2025, redeem the 2025 CQP Senior Notes, in whole or in part, at the redemption prices set forth in the CQP Indenture.

The 2025 CQP Senior Notes are our senior obligations, ranking equally in right of payment with our other existing and future unsubordinated debt and senior to any of our future subordinated debt. The 2025 CQP Senior Notes will be secured alongside the 2016 CQP Credit Facilities on a first-priority basis (subject to permitted encumbrances) with liens on (1) substantially all the existing and future tangible and intangible assets and our rights and the rights of the CQP Guarantors and equity interests in the CQP Guarantors (except, in each case, for certain excluded properties set forth in the 2016 CQP Credit Facilities) and (2) substantially all of the real property of SPLNG (except for excluded properties referenced in the 2016 CQP Credit Facilities). The liens securing the 2025 CQP Senior Notes would be released if (1) the aggregate principal amount of all indebtedness then outstanding under the term loans under the 2016 CQP Credit Facilities secured by such liens does not exceed $1.0 billion and (2) the aggregate amount of our secured indebtedness and the secured indebtedness of the CQP Guarantors (other than the 2025 CQP Senior Notes or any other series of notes issued under the CQP Indenture) outstanding at any one time, together with all Attributable Indebtedness (as defined in the CQP Indenture) from sale-leaseback transactions (subject to certain exceptions), does not exceed the greater of (1) $1.5 billion and (2) 10% of net tangible assets. Upon the release of the liens securing the 2025 CQP Senior Notes, the limitation on liens covenant under the CQP Indenture will continue to govern the incurrence of liens by us and the CQP Guarantors.

In connection with the closing of the sale of the 2025 CQP Senior Notes, we and the CQP Guarantors entered into a registration rights agreement (the “CQP Registration Rights Agreement”). Under the CQP Registration Rights Agreement, we and the CQP Guarantors have agreed to use commercially reasonable efforts to file with the SEC and cause to become effective a registration statement relating to an offer to exchange any and all of the 2025 CQP Senior Notes for a like aggregate principal amount of our debt securities with terms identical in all material respects to the 2025 CQP Senior Notes sought to be exchanged (other than with respect to restrictions on transfer or to any increase in annual interest rate), within 360 days after September 18, 2017. Under specified circumstances, we and the CQP Guarantors have also agreed to use commercially reasonable efforts to cause to become effective a shelf registration statement relating to resales of the 2025 CQP Senior Notes. We will be obligated to pay additional interest on the 2025 CQP Senior Notes if we fail to comply with our obligation to register the 2025 CQP Senior Notes within the specified time period.

Credit Facilities

Below is a summary of our credit facilities outstanding as of December 31, 2017 (in millions):

|

| | | | | | | | |

| | SPL Working Capital Facility | | 2016 CQP Credit Facilities |

Original facility size | | $ | 1,200 |

| | $ | 2,800 |

|

Less: | | | | |

Outstanding balance | | — |

| | 1,090 |

|

Commitments prepaid or terminated | | — |

| | 1,470 |

|

Letters of credit issued | | 730 |

| | 20 |

|

Available commitment | | $ | 470 |

|

| $ | 220 |

|

| | | | |

Interest rate | | LIBOR plus 1.75% or base rate plus 0.75% | | LIBOR plus 2.25% or base rate plus 1.25% (1) |

Maturity date | | December 31, 2020, with various terms for underlying loans | | February 25, 2020, with principal payments due quarterly commencing on March 31, 2019 |

| |

(1) | There is a 0.50% step-up for both LIBOR and base rate loans beginning on February 25, 2019. |

SPL Working Capital Facility

In September 2015, SPL entered into the SPL Working Capital Facility, which is intended to be used for loans to SPL (“Working Capital Loans”), the issuance of letters of credit on behalf of SPL, as well as for swing line loans to SPL (“Swing Line Loans”), primarily for certain working capital requirements related to developing and placing into operation the Liquefaction Project. SPL may, from time to time, request increases in the commitments under the SPL Working Capital Facility of up to $760 million and, upon the completion of the debt financing of Train 6 of the Liquefaction Project, request an incremental increase in commitments of up to an additional $390 million.

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

Loans under the SPL Working Capital Facility accrue interest at a variable rate per annum equal to LIBOR or the base rate (equal to the highest of the senior facility agent’s published prime rate, the federal funds effective rate, as published by the Federal Reserve Bank of New York, plus 0.50% and one month LIBOR plus 0.50%), plus the applicable margin. The applicable margin for LIBOR loans under the SPL Working Capital Facility is 1.75% per annum, and the applicable margin for base rate loans under the SPL Working Capital Facility is 0.75% per annum. Interest on Swing Line Loans and loans deemed made in connection with a draw upon a letter of credit (“LC Loans”) is due and payable on the date the loan becomes due. Interest on LIBOR loans is due and payable at the end of each applicable LIBOR period, and interest on base rate loans is due and payable at the end of each fiscal quarter. However, if such base rate loan is converted into a LIBOR loan, interest is due and payable on that date. Additionally, if the loans become due prior to such periods, the interest also becomes due on that date.

SPL pays (1) a commitment fee equal to an annual rate of 0.70% on the average daily amount of the excess of the total commitment amount over the principal amount outstanding without giving effect to any outstanding Swing Line Loans and (2) a letter of credit fee equal to an annual rate of 1.75% of the undrawn portion of all letters of credit issued under the SPL Working Capital Facility. If draws are made upon a letter of credit issued under the SPL Working Capital Facility and SPL does not elect for such draw (an “LC Draw”) to be deemed an LC Loan, SPL is required to pay the full amount of the LC Draw on or prior to the business day following the notice of the LC Draw. An LC Draw accrues interest at an annual rate of 2.0% plus the base rate. As of December 31, 2017, no LC Draws had been made upon any letters of credit issued under the SPL Working Capital Facility.

The SPL Working Capital Facility matures on December 31, 2020, and the outstanding balance may be repaid, in whole or in part, at any time without premium or penalty upon three business days’ notice. LC Loans have a term of up to one year. Swing Line Loans terminate upon the earliest of (1) the maturity date or earlier termination of the SPL Working Capital Facility, (2) the date 15 days after such Swing Line Loan is made and (3) the first borrowing date for a Working Capital Loan or Swing Line Loan occurring at least three business days following the date the Swing Line Loan is made. SPL is required to reduce the aggregate outstanding principal amount of all Working Capital Loans to zero for a period of five consecutive business days at least once each year.