UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

|

| |

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2012

OR

|

| |

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File No. 001-33366

CHENIERE ENERGY PARTNERS, L.P.

(Exact name of registrant as specified in its charter)

|

| | |

Delaware | | 20-5913059 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| | |

700 Milam Street, Suite 800 | | |

Houston, Texas | | 77002 |

(Address of principal executive offices) | | (Zip code) |

Registrant’s telephone number, including area code: (713) 375-5000

Securities registered pursuant to Section 12(b) of the Act:

|

| |

Common Units Representing Limited Partner Interests | NYSE MKT |

(Title of Class) | (Name of each exchange on which registered) |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

|

| | |

Large accelerated filer o | | Accelerated filer x |

Non-accelerated filer o | | Smaller reporting company o |

(Do not check if a smaller reporting company) | | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

The aggregate market value of the registrant’s Common Units held by non-affiliates of the registrant was approximately $439 million as of June 30, 2012.

The issuer had 39,488,488 common units, 133,333,334 Class B units and 135,383,831 subordinated units outstanding as of February 13, 2013.

Documents incorporated by reference: None

CHENIERE ENERGY PARTNERS, L.P

TABLE OF CONTENTS

CAUTIONARY STATEMENT

REGARDING FORWARD-LOOKING STATEMENTS

This annual report contains certain statements that are, or may be deemed to be, "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933, as amended (the "Securities Act"), and Section 21E of the Securities Exchange Act of 1934, as amended (the "Exchange Act"). All statements, other than statements of historical facts, included herein or incorporated herein by reference are "forward-looking statements." Included among "forward-looking statements" are, among other things:

| |

• | statements regarding our ability to pay distributions to our unitholders; |

| |

• | statements regarding our expected receipt of cash distributions from Sabine Pass LNG, L.P. ("Sabine Pass LNG") or Sabine Pass Liquefaction, LLC ("Sabine Pass Liquefaction"); |

| |

• | statements regarding future levels of domestic and international natural gas production, supply or consumption or future levels of liquefied natural gas ("LNG") imports into or exports from North America and other countries worldwide, regardless of the source of such information, or the transportation or demand for and prices related to natural gas, LNG or other hydrocarbon products; |

| |

• | statements regarding any financing transactions or arrangements, or ability to enter into such transactions; |

| |

• | statements relating to the construction of our Trains, including statements concerning the engagement of any engineering, procurement and construction ("EPC") contractor or other contractor and the anticipated terms and provisions of any agreement with any EPC or other contractor, and anticipated costs related thereto; |

| |

• | statements regarding any agreement to be entered into or performed substantially in the future, including any revenues anticipated to be received and the anticipated timing thereof, and statements regarding the amounts of total LNG regasification, liquefaction or storage capacities that are, or may become subject to contracts; |

| |

• | statements regarding counterparties to our commercial contracts, construction contracts and other contracts; |

| |

• | statements regarding our planned construction of additional Trains, including the financing of such Trains; |

| |

• | statements that our Trains, when completed, will have certain characteristics, including amounts of liquefaction capacities; |

| |

• | statements regarding our business strategy, our strengths, our business and operation plans or any other plans, forecasts, projections or objectives, including anticipated revenues and capital expenditures, any or all of which are subject to change; |

| |

• | statements regarding legislative, governmental, regulatory, administrative or other public body actions, requirements, permits, investigations, proceedings or decisions; |

| |

• | statements regarding our anticipated LNG and natural gas marketing activities; and |

| |

• | any other statements that relate to non-historical or future information. |

These forward-looking statements are often identified by the use of terms and phrases such as "achieve," "anticipate," "believe," "contemplate," "develop," "estimate," "expect," "forecast," "plan," "potential," "project," "propose," "strategy" and similar terms and phrases, or by the use of future tense. Although we believe that the expectations reflected in these forward-looking statements are reasonable, they do involve assumptions, risks and uncertainties, and these expectations may prove to be incorrect. You should not place undue reliance on these forward-looking statements, which are made as of the date of this annual report and speak only as of the date of this annual report.

Our actual results could differ materially from those anticipated in these forward-looking statements as a result of a variety of factors, including those discussed in "Risk Factors." All forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by these risk factors.

DEFINITIONS

In this annual report, unless the context otherwise requires:

| |

• | Bcf means billion cubic feet; |

| |

• | Bcf/d means billion cubic feet per day; |

| |

• | Bcfe means billion cubic feet of natural gas equivalent using the ratio of six thousand cubic feet of natural gas to one barrel (or 42 U.S. gallons liquid volume) of crude oil, condensate and natural gas liquids; |

| |

• | Dthd means dekatherms per day which is equivalent to one million British thermal units or one MMBtu per day; |

| |

• | EPC means engineering, procurement and construction; |

| |

• | Henry Hub means the final settlement price (in USD per MMBtu) for the New York Mercantile Exchange's Henry Hub natural gas futures contract for the month in which a relevant cargo's delivery window is scheduled to begin; |

| |

• | LNG means liquefied natural gas; |

| |

• | MMBtu means million British thermal units; |

| |

• | mmtpa means million metric tons per annum; |

| |

• | SPA means a LNG sale and purchase agreement; |

| |

• | Tcf means trillion cubic feet; |

| |

• | Train means a natural gas liquefaction train; and |

| |

• | TUA means terminal use agreement. |

PART I

ITEMS 1. and 2. BUSINESS AND PROPERTIES

General

We are a Delaware limited partnership formed by Cheniere Energy, Inc. ("Cheniere"). Through our wholly owned subsidiary, Sabine Pass LNG, we own and operate the regasification facilities at the Sabine Pass LNG terminal located on the Sabine Pass deep water shipping channel less than four miles from the Gulf Coast. The Sabine Pass LNG terminal includes existing infrastructure of five LNG storage tanks with capacity of approximately 16.9 Bcfe, two docks that can accommodate vessels of up to 265,000 cubic meters and vaporizers with regasification capacity of approximately 4.0 Bcf/d. Approximately one-half of the LNG receiving capacity at the Sabine Pass LNG terminal is contracted to two multinational energy companies. We are developing natural gas liquefaction facilities (the "Liquefaction Project") at the Sabine Pass LNG terminal adjacent to the existing regasification facilities through a wholly owned subsidiary, Sabine Pass Liquefaction. Unless the context requires otherwise, references to "Cheniere Partners", "we", "us" and "our" refer to Cheniere Energy Partners, L.P. and its subsidiaries, including Sabine Pass LNG and Sabine Pass Liquefaction.

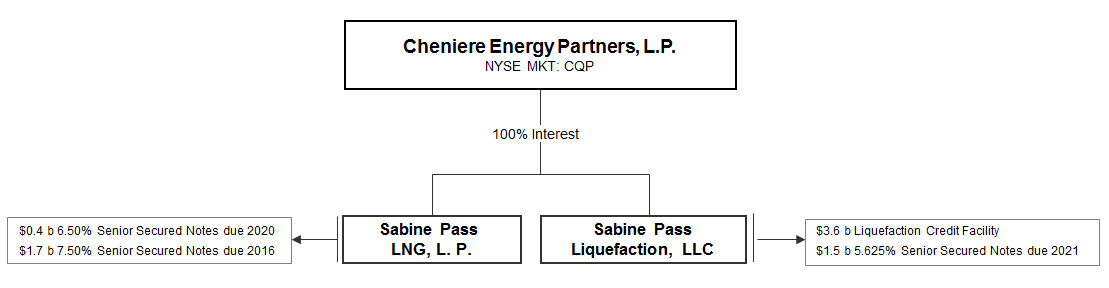

The following diagram depicts our abbreviated capital structure, including our ownership of Sabine Pass LNG and Sabine Pass Liquefaction as of February 13, 2013:

LNG is natural gas that, through a refrigeration process, has been cooled to a liquid state, which occupies a volume that is approximately 1/600th of its gaseous state. The liquefaction of natural gas into LNG allows it to be shipped economically from areas of the world where natural gas is abundant and inexpensive to produce to other areas where natural gas demand and infrastructure exist to justify economically the use of LNG. LNG is transported using large oceangoing LNG tankers specifically constructed for this purpose. LNG receiving terminals offload LNG from LNG tankers, store the LNG prior to processing, heat the LNG to return it to a gaseous state and deliver the resulting natural gas into pipelines for transportation to market.

Our Business Strategy

Our primary business strategy is to develop, construct, and operate assets supported by long-term, fixed fee contracts. We plan to implement our strategy by:

| |

• | completing construction and commencing operation of our Trains (each in sequence, "Train 1", "Train 2", "Train 3", "Train 4", "Train 5" and "Train 6"); |

| |

• | developing and operating our Trains safely, efficiently and reliably; |

| |

• | making LNG available to our long-term SPA customers to generate steady and reliable revenues and operating cash flows; |

| |

• | safely maintaining and operating the Sabine Pass LNG terminal; |

| |

• | utilizing capacity at the Sabine Pass LNG terminal for short-term and spot LNG purchases and sales until such capacity is used in connection with the Liquefaction Project; |

| |

• | developing business relationships for the marketing of additional long-term and short-term agreements for excess LNG volumes at the Sabine Pass LNG terminal that have not been sold to our long-term customers, and for long-term and short-term contracts for potential future projects at other sites; and |

| |

• | expanding our existing asset base through acquisitions from Cheniere or third parties or our own development of the Liquefaction Project or complementary businesses or assets such as other LNG terminals, natural gas storage assets and natural gas pipelines. |

Our Business

We have constructed and are operating the Sabine Pass LNG terminal located on the Sabine Pass deep water shipping channel less than four miles from the Gulf Coast. We have long-term leases for five tracts of land consisting of 1,044 acres. We are currently operating LNG receiving facilities at the terminal and are developing and constructing the Liquefaction Project.

Regasification Facilities

The regasification facilities at the Sabine Pass LNG terminal have operational regasification capacity of approximately 4.0 Bcf/d and aggregate LNG storage capacity of approximately 16.9 Bcfe. Approximately 2.0 Bcf/d of the regasification capacity at the Sabine Pass LNG terminal has been reserved under two long-term third-party TUAs, under which Sabine Pass LNG’s customers are required to pay fixed monthly fees, whether or not they use the LNG terminal. Capacity reservation fee TUA payments are made by Sabine Pass LNG's third-party TUA customers as follows:

| |

• | Total Gas & Power North America, Inc. ("Total") has reserved approximately 1.0 Bcf/d of regasification capacity and is obligated to make monthly capacity payments to Sabine Pass LNG aggregating approximately $125 million per year for 20 years that commenced April 1, 2009. Total, S.A. has guaranteed Total’s obligations under its TUA up to $2.5 billion, subject to certain exceptions; and |

| |

• | Chevron U.S.A. Inc. ("Chevron") has reserved approximately 1.0 Bcf/d of regasification capacity and is obligated to make monthly capacity payments to Sabine Pass LNG aggregating approximately $125 million per year for 20 years that commenced July 1, 2009. Chevron Corporation has guaranteed Chevron’s obligations under its TUA up to 80% of the fees payable by Chevron. |

The remaining approximately 2.0 Bcf/d of capacity has been reserved under a TUA by Sabine Pass Liquefaction. Sabine Pass Liquefaction is obligated to make monthly capacity payments to Sabine Pass LNG aggregating approximately $250 million per year, continuing until at least 20 years after Sabine Pass Liquefaction delivers its first commercial cargo at Sabine Pass Liquefaction's facilities under construction, which may occur as early as late 2015. Sabine Pass Liquefaction obtained this reserved capacity as a result of an assignment in July 2012 by Cheniere Energy Investments, LLC ("Cheniere Investments"), a wholly owned subsidiary of Cheniere Partners, of its rights, title and interest under its TUA. In connection with the assignment, Sabine Pass Liquefaction, Cheniere Investments and Sabine Pass LNG entered into a terminal use rights assignment and agreement ("TURA") pursuant to which Cheniere Investments has the right to use Sabine Pass Liquefaction's reserved capacity under the TUA and has the obligation to make the monthly capacity payments required by the TUA to Sabine Pass LNG. In an effort to monetize Cheniere Investments' reserved capacity under its TURA during construction of the Liquefaction Project, Cheniere Marketing, LLC ("Cheniere Marketing"), a wholly owned subsidiary of Cheniere, has entered into a variable capacity rights agreement ("VCRA") pursuant to which Cheniere Marketing is obligated to pay Cheniere Investments 80% of the expected gross margin of each cargo of LNG that Cheniere Marketing arranges for delivery to the Sabine Pass LNG terminal. The revenue earned by Sabine Pass LNG from the capacity payments made under the TUA and the revenue earned by Cheniere Investments under the VCRA are eliminated upon consolidation of our financial statements. We have guaranteed the obligations of Sabine Pass Liquefaction under its TUA and the obligations of Cheniere Investments under the TURA.

In September 2012, Sabine Pass Liquefaction entered into a partial TUA assignment agreement with Total, whereby Sabine Pass Liquefaction will progressively gain access to Total's capacity and other services provided under Total's TUA with Sabine Pass LNG. This agreement will provide Sabine Pass Liquefaction with additional berthing and storage capacity at the Sabine Pass LNG terminal that may be used to accommodate the development of Train 5 and Train 6, provide increased flexibility in managing LNG cargo loading and unloading activity starting with the commencement of commercial operations of Train 3, and permit Sabine Pass Liquefaction to more flexibly manage its LNG storage capacity with the commencement of Train 1. Notwithstanding any arrangements between Total and Sabine Pass Liquefaction, payments required to be made by Total to Sabine Pass LNG shall continue to be made by Total to Sabine Pass LNG in accordance with its TUA.

Under each of these TUAs, Sabine Pass LNG is entitled to retain 2% of the LNG delivered to the Sabine Pass LNG terminal.

Liquefaction Facilities

The Liquefaction Project is being developed at the Sabine Pass LNG terminal adjacent to the existing regasification facilities. We plan to construct up to six Trains, which are in various stages of development. We have commenced construction of Train 1 and Train 2 and the related new facilities needed to treat, liquefy, store and export natural gas. Construction of Train 3 and Train 4 and the related facilities is expected to commence upon, among other things, obtaining financing commitments sufficient to fund construction of such Trains and making a positive final investment decision. We recently began the development of Train 5 and Train 6 and expect to commence the regulatory approval process in the first half of 2013.

The Trains are being designed, constructed and commissioned by Bechtel Oil, Gas and Chemicals, Inc. ("Bechtel") using the ConocoPhillips Optimized Cascade® technology, a proven technology deployed in numerous LNG projects around the world. Sabine Pass Liquefaction has entered into lump sum turnkey contracts for the engineering, procurement and construction of Train 1 and Train 2 (the "EPC Contract (Train 1 and 2)") and Train 3 and Train 4 (the "EPC Contract (Train 3 and 4)", and together with the EPC Contract (Train 1 and 2), the "EPC Contracts"), with Bechtel in November 2011 and December 2012, respectively.

In August 2012, we received a final order from the U.S. Department of Energy ("DOE") to export 16 mmtpa of LNG to all nations with which trade is permitted. In April 2012, we received authorization from the Federal Energy Regulatory Commissin ("FERC") to site, construct and operate Train 1, Train 2, Train 3 and Train 4.

As of December 31, 2012, the overall project completion for Train 1 and Train 2 was approximately 18% complete. Based on our current construction schedule, we anticipate that Train 1 will produce LNG as early as the end of 2015.

Customers

As of February 13, 2013, Sabine Pass Liquefaction has entered into the following third-party SPAs:

| |

• | BG Gulf Coast LNG, LLC ("BG") SPA commences upon the date of first commercial delivery for Train 1 and includes an annual contract quantity of 182,500,000 MMBtu of LNG and a fixed fee of $2.25 per MMBtu and includes additional annual contract quantities of 36,500,000 MMBtu, 34,000,000 MMBtu, and 33,500,000 MMBtu upon the date of first commercial delivery for Train 2, Train 3 and Train 4, respectively, with a fixed fee of $3.00 per MMBtu. The total expected annual contracted cash flow from BG from the fixed fee component is $723 million. In addition, Sabine Pass Liquefaction has agreed to make LNG available to BG to the extent that Train 1 becomes commercially operable prior to the beginning of the first delivery window. The obligations of BG are guaranteed by BG Energy Holdings Limited, a company organized under the laws of England and Wales, with a credit rating of A2/A. |

| |

• | Gas Natural Aprovisionamientos SDG S.A. ("Gas Natural Fenosa"), an affiliate of Gas Natural SDG, S.A., SPA commences upon the date of first commercial delivery for Train 2 and includes an annual contract quantity of 182,500,000 MMBtu of LNG and a fixed fee of $2.49 per MMBtu, equating to expected annual contracted cash flow from the fixed fee component of $454 million. The obligations of Gas Natural Fenosa are guaranteed by Gas Natural SDG S.A., a company organized under the laws of Spain, with a credit rating of Baa2/BBB. |

| |

• | Korea Gas Corporation ("KOGAS") SPA commences upon the date of first commercial delivery for Train 3 and includes an annual contract quantity of 182,500,000 MMBtu of LNG and a fixed fee of $3.00 per MMBtu, equating to expected annual contracted cash flow from fixed fees of $548 million. KOGAS is organized under the laws of the Republic of Korea, with a credit rating of A/A1. |

| |

• | GAIL (India) Limited ("GAIL") SPA commences upon the date of first commercial delivery for Train 4 and includes an annual contract quantity of 182,500,000 MMBtu of LNG and a fixed fee of $3.00 per MMBtu, equating to expected annual contracted cash flow from fixed fees of $548 million. GAIL is organized under the laws of India, with a credit rating of Baa2/BBB-. |

| |

• | Total, an affiliate of Total S.A., SPA commences upon the date of first commercial delivery for Train 5 and includes an annual contract quantity of 104,750,000 MMBtu of LNG and a fixed fee of $3.00 per MMBtu, equating to expected annual contracted cash flow from fixed fees of $314 million. The obligations of Total are guaranteed by Total S.A., a company organized under the laws of France, with a credit rating of Aa1/AA. |

In aggregate, the fixed fee portion to be paid by these customers is approximately $2.6 billion annually, with fixed fees starting from the commencement of operations of Train 1, Train 2, Train 3, Train 4 and Train 5 equating to $411 million, $564 million, $650 million, $648 million and $314 million, respectively.

In addition, Cheniere Marketing has entered into an SPA to purchase, at its option, any excess LNG produced that is not committed to non-affiliate parties, for up to a maximum of 104,000,000 MMBtu per annum produced from Train 1 through Train 4. Cheniere Marketing may purchase incremental LNG volumes at a price of 115% of Henry Hub plus up to $3.00 per MMBtu for the first 36,000,000 MMBtu of the most profitable cargoes sold each year by Cheniere Marketing, and then 20% of net profits of the remaining 68,000,000 MMBtu sold each year by Cheniere Marketing.

Construction

In November 2011, Sabine Pass Liquefaction entered into the EPC Contract (Train 1 and 2) with Bechtel. Sabine Pass Liquefaction issued a notice to proceed for construction under the EPC Contract (Train 1 and 2) in August 2012.

In December 2012, Sabine Pass Liquefaction entered into the EPC Contract (Train 3 and 4) with Bechtel. Under the EPC Contract (Train 3 and 4), if Sabine Pass Liquefaction fails to issue notice to proceed to Bechtel by December 31, 2013, then either Sabine Pass Liquefaction or Bechtel may terminate the EPC Contract (Train 3 and 4), and Bechtel will be paid costs reasonably incurred on account of such termination and a lump sum of $5.0 million. The Trains are in various stages of development, as described above.

The contract price of the EPC Contract (Train 1 and 2) is approximately $3.97 billion, reflecting amounts incurred under change orders through December 31, 2012. Total expected capital costs for Train 1 and Train 2 are estimated to be between $4.5 billion and $5.0 billion before financing costs, including estimated owner's costs and contingencies. Budgeted total all-in costs for Train 1 and Train 2 are estimated to be between $5.5 billion and $6.0 billion, including financing costs and interest expense during construction. The contract price of the EPC Contract (Train 3 and 4) is $3.77 billion, only subject to adjustment by change order (including if Sabine Pass Liquefaction issues the notice to proceed after June 1, 2013). The cost to construct Train 3 and Train 4 is currently estimated to be between $4.5 billion and $5.0 billion before financing costs, including estimated owner's costs and contingencies.

The liquefaction technology to be employed under the EPC Contracts is the ConocoPhillips Optimized Cascade® Process, which was first used at the ConocoPhillips Petroleum Kenai plant built by Bechtel in 1969 in Kenai, Alaska. Bechtel has since designed and/or constructed LNG facilities using the ConocoPhillips Optimized Cascade® technology in Angola, Australia, Egypt, Equatorial Guinea and Trinidad. The design and technology has been proven in over four decades of operation.

Pipeline Facilities

Cheniere Creole Trail Pipeline, L.P. ("Creole Trail"), an indirect wholly owned subsidiary of Cheniere, owns the Creole Trail Pipeline, a 94-mile pipeline interconnecting the Sabine Pass LNG terminal with a number of large interstate pipelines, including Natural Gas Pipeline Company of America, Transcontinental Gas Pipeline Corporation, Tennessee Gas Pipeline Company, Florida Gas Transmission Company, Texas Eastern Gas Transmission, and Trunkline Gas Company, as well as the intrastate pipeline system of Bridgeline Holdings, L.P.

Sabine Pass Liquefaction has entered into a transportation precedent agreement to secure firm pipeline transportation capacity with Creole Trail and two other pipelines for Train 1 and Train 2. Creole Trail filed an application with the FERC in April 2012 for certain modifications to allow the Creole Trail Pipeline to be able to transport natural gas to the Sabine Pass LNG terminal. Creole Trail estimates the capital costs to modify the Creole Trail Pipeline will be approximately $90 million. The modifications are expected to be in service in time for the commissioning and testing of Train 1 and Train 2.

We have entered into an agreement with Cheniere to purchase the equity interests of the entities that own the Creole Trail Pipeline if, among other things, we obtain acceptable financing for the purchase price. The consideration to be paid by us for the Creole Trail Pipeline is 12 million Class B units and $300 million, plus any costs incurred by Creole Trail from August 2012 until the purchase date, including, if applicable, any portion of the expected $90 million for pipeline modifications.

LNG Terminal Governmental Regulation

The Sabine Pass LNG terminal and Liquefaction Project operations and construction are subject to extensive regulation under federal, state and local statutes, rules, regulations and laws. These laws require that we engage in consultations with appropriate federal and state agencies and that we obtain and maintain applicable permits and other authorizations. This regulatory burden increases our cost of operations and construction, and failure to comply with such laws could result in substantial penalties.

Federal Energy Regulatory Commission ("FERC")

The design, construction and operation of our proposed liquefaction facilities, and the export of LNG, are highly regulated activities. In order to site and construct the Sabine Pass LNG terminal, we received and are required to maintain authorization from the FERC under Section 3 of the Natural Gas Act of 1938, as amended ("NGA"). The FERC's approval under Section 3 of the NGA, as well as several other material governmental and regulatory approvals and permits, are required in order to site, construct and operate our liquefaction facilities.

The Energy Policy Act of 2005 ("EPAct"), amended Section 3 of the NGA to establish or clarify the FERC's exclusive authority to approve or deny an application for the siting, construction, expansion or operation of LNG terminals, although except as specifically provided in the EPAct, nothing in the EPAct is intended to affect otherwise applicable law related to any other federal agency's authorities or responsibilities related to LNG terminals. Sabine Pass Liquefaction filed an application with the FERC in January 2011 for an order under Section 3 of the NGA authorizing the siting, construction and operation of the Liquefaction Project, including the siting, construction and operation of Train 1 through Train 4. The FERC issued final orders in April and July

2012 approving Sabine Pass Liquefaction's application. Subsequently, the FERC issued written approval to commence site preparation work for Train 1 through Train 4. The FERC approval requires Sabine Pass Liquefaction to obtain certain additional FERC approvals as construction progresses. To date Sabine Pass Liquefaction has been able to obtain these approvals as needed. In October 2012, Sabine Pass Liquefaction filed an application at the FERC to amend its orders to reflect certain modifications of the Liquefaction Project. The pending modifications will require additional review by the FERC under the National Environmental Policy Act ("NEPA"), which will include preparation and evaluation of a supplemental Environmental Assessment for the project. The need for this approval has not materially affected Sabine Pass Liquefaction's construction progress. Sabine Pass Liquefaction will also need the FERC's approval to construct Train 5 and Train 6, which have not yet been authorized at this time. Throughout the life of our proposed liquefaction facilities, we will be subject to regular reporting requirements to the FERC and the U.S. Department of Transportation regarding the operation and maintenance of the facilities.

The EPAct amended the NGA to prohibit market manipulation, and increased civil and criminal penalties for any violations of the NGA and any rules, regulations or orders of the FERC, up to $1.0 million per day per violation. In accordance with the EPAct, the FERC issued a final rule making it unlawful for any entity, in connection with the purchase or sale of natural gas or transportation service subject to the FERC's jurisdiction, to defraud, make an untrue statement or omit a material fact or engage in any practice, act or course of business that operates or would operate as a fraud.

DOE Export License

The DOE has issued two orders authorizing exports from the Liquefaction Project: an order authorizing the export of up to the equivalent of 16 mmtpa (approximately 803 Bcf) of domestically produced LNG by vessel from the Sabine Pass LNG terminal to countries with which the United States has a Free Trade Agreement providing for national treatment for trade in natural gas ("FTA") for a 30-year term, beginning on the earlier of the date of first export or September 7, 2020, and another order authorizing the export of up to the equivalent of 803 Bcf per year (approximately 16 mmtpa) of domestically produced LNG by vessel from the Sabine Pass LNG terminal to non-FTA countries for a 20-year term, beginning on the earlier of the date of first export or August 7, 2017.

Exports of natural gas to countries with which the United States has an FTA are "deemed to be consistent with the public interest" and authorization to export LNG to FTA countries shall be granted by the DOE without "modification or delay". Sabine Pass Liquefaction received approval to export to FTA countries in September 2010. FTA countries which import LNG now or will do so by 2016 include: Chile, Mexico, Singapore, South Korea and the Dominican Republic.

Exports of natural gas to countries with which the United States does not have an FTA are considered by DOE in the context of a comment period whereby interveners are provided the opportunity to assert that such authorization would not be consistent with the public interest. Sabine Pass Liquefaction received final approval to export to non-FTA countries in August 2012.

Other Governmental Permits, Approvals and Authorizations

The operation of the Sabine Pass LNG terminal and related projects, and the construction and operation of our proposed liquefaction facilities, are also subject to additional federal permits, orders, approvals and consultations required by other federal agencies, including: the DOE, Advisory Council on Historic Preservation, U.S. Army Corps of Engineers, U.S. Department of Commerce, National Marine Fisheries Services, U.S. Department of the Interior, U.S. Fish and Wildlife Service, EPA and U.S. Department of Homeland Security.

Three significant permits are the U.S. Army Corps of Engineers ("USACE") Section 404 of the Clean Water Act/Section 10 of the Rivers and Harbors Act Permit (the "Section 10/404 Permit"), the Clean Air Act Title V Operating Permit and the Prevention of Significant Deterioration (PSD) Permit, the latter two permits issued by the Louisiana Department of Environmental Quality ("LDEQ").

The application for revision of the Sabine Pass LNG terminal's Section 10/404 Permit to authorize construction of Train 1 through Train 4 was submitted in January 2011. The process included a public comment period which commenced in March 2011 and closed in April 2011. The revised Section 10/404 permit was received from the USACE in March 2012. The USACE acted in the capacity as a cooperating agency in the FERC's NEPA review process. The application to amend the Sabine Pass LNG terminal's existing Title V and PSD permits to authorize construction of Train 1 through Train 4 was initially submitted in December 2010 and revised in March 2011. The process included a public comment period from June 2011 to August 2011 and a public

hearing in August 2011. The final revised Title V and PSD permits were issued by the LDEQ in December 2011. Although this permit is final, a petition with the EPA has been filed pursuant to the Clean Air Act requesting that the EPA object to the Title V permit. EPA has not ruled on this petition. In June 2012, we applied to the LDEQ for a further amendment to the Title V and PSD permits to reflect the proposed modifications to the Liquefaction Project that were filed with the FERC in October 2012 as discussed above. In November 2012, the LDEQ issued proposed revised air permits for public comment, and comments regarding the proposed revised air permits have been filed. We anticipate, but cannot guarantee, that the revised Title V and PSD permits will be issued during the first quarter of 2013.

We will also need to obtain a modification to the Sabine Pass LNG terminal's existing wastewater discharge permit to authorize discharges from the liquefaction facilities prior to the commencement of operation of the Liquefaction Project.

The Sabine Pass LNG terminal regasification and liquefaction facilities are subject to U.S. Department of Transportation safety regulations and standards for the transportation and storage of LNG and regulations of the U.S. Coast Guard relating to maritime safety and facility security.

Commodity Futures Trading Commission

Congress adopted comprehensive financial reform legislation that establishes federal oversight and regulation of the over-the-counter derivatives market and entities, such as us, that participate in that market. This legislation, known as the Dodd-Frank Wall Street Reform and Consumer Protection Act (the "Dodd-Frank Act"), is designed primarily to (1) regulate certain participants in the swaps markets, including new entities defined as "Swap Dealers" and "Major Swap Participants," (2) require clearing and exchange-trading of certain swaps that the Commodities Futures Trading Commission (the "CFTC") determines must be cleared, (3) increase swap market transparency through robust reporting and recordkeeping requirements, and (4) enhance the CFTC's rulemaking and enforcement authority, including the authority to establish position limits on swaps products. This legislation requires the CFTC, the SEC and other regulators to promulgate rules and regulations implementing the Dodd-Frank Act. In November 2011, the CFTC adopted rules to impose new position limits on certain core futures and equivalent swaps contracts for physical commodities, including natural gas, with exceptions for certain bona fide hedging transactions. These new position limit rules were vacated by a federal district court in September 2012, and the CFTC has appealed this ruling. Consequently, the CFTC's vacated position limits rules will not go into effect unless and until the CFTC prevails on appeal of this ruling or issues and finalizes revised rules.

In October 2012, the CFTC's and SEC's joint rules further defining the term "swap" became effective, which triggered the start of certain Dodd-Frank Act regulatory obligations. The CFTC's swaps reporting and recordkeeping rules are to be phased in over 180 days following October 12, 2012, depending on swap asset class and counterparty. It is expected that entities that are end users of swaps or otherwise are not swap dealers or major swap participants will be required to comply with the Dodd-Frank Act reporting and recordkeeping rules in April 2013. In December 2012, the CFTC published final rules regarding mandatory clearing of certain interest rate swaps and certain index credit default swaps and setting compliance dates for different categories of market participants, the earliest of which is March 11, 2013. The CFTC has not yet proposed any rules requiring the clearing of any other classes of swaps, including physical commodity swaps. Although we expect to qualify for the end-user exception from the clearing requirement for our swaps, mandatory clearing requirements applicable to other market participants, such as swap dealers, may change the cost and availability of the swaps that we use for hedging. For uncleared swaps, the Dodd-Frank Act may also require our counterparties to require that we enter into credit support documentation and/or initial and variation margin requirements; however, the CFTC's and other agencies' margin rules are not yet final and therefore the application of those provisions to us is uncertain at this time. The financial reform legislation may also cause our derivatives counterparties to spin off some of their derivatives activities to a separate entity, which may not be as creditworthy as the current counterparty. The new legislation, and any additional regulations, may also adversely affect our existing derivative contracts and restrict our ability to monetize such contracts, cause us to restructure certain contracts, reduce the availability of derivatives to protect against risks or to optimize assets, and impact the liquidity of certain swaps products, all of which could increase our business costs.

LNG Terminal Environmental Regulation

Our LNG terminal operations, including the proposed liquefaction facilities, are subject to various federal, state and local laws and regulations relating to the protection of the environment. These environmental laws and regulations may impose substantial penalties for noncompliance and substantial liabilities for pollution. Many of these laws and regulations restrict or prohibit the

types, quantities and concentration of substances that can be released into the environment and can lead to substantial civil and criminal fines and penalties for non-compliance.

Clean Air Act ("CAA")

Our LNG terminal operations, including the proposed liquefaction facilities, are subject to the federal CAA and comparable state and local laws. We may be required to incur certain capital expenditures over the next several years for air pollution control equipment in connection with maintaining or obtaining permits and approvals addressing air emission-related issues. We do not believe, however, that our operations, or the construction and operations of our proposed liquefaction facilities, will be materially and adversely affected by any such requirements.

In 2009, the EPA promulgated and finalized the Mandatory Greenhouse Gas Reporting Rule for multiple sections of the economy. This rule requires mandatory reporting of greenhouse gas ("GHG") emissions from stationary fuel combustion sources as well as all fugitive emissions throughout LNG terminals. From time to time, Congress has considered proposed legislation directed at reducing GHG emissions, and the EPA has defined GHG emissions thresholds for requiring certain permits for new and existing industrial sources. It is not possible at this time to predict how future regulations or legislation may address GHG emissions and impact our business. However, future regulations and laws could result in increased compliance costs or additional operating restrictions and could have a material adverse effect on our business, financial position, results of operations and cash flows.

Coastal Zone Management Act ("CZMA")

Our LNG terminals, including the proposed liquefaction facilities, are subject to the review and possible requirements of the CZMA throughout the construction of facilities located within the coastal zone. The CZMA is administered by the states (in Louisiana, by the Department of Natural Resources, and in Texas, by the General Land Office). This program is implemented to ensure that impacts to coastal areas are consistent with the intent of the CZMA to manage the coastal areas.

Clean Water Act ("CWA")

The Sabine Pass LNG terminal operations and the proposed liquefaction facilities are subject to the federal CWA and analogous state and local laws. The CWA imposes strict controls on the discharge of pollutants into the navigable waters of the United States, including discharges of wastewater and storm water runoff and fill/discharges into waters of the United States. Permits must be obtained to discharge pollutants into state and federal waters. The CWA is administered by the EPA, the USACE, and by the states (in Louisiana, by the LDEQ, and in Texas, by the Texas Commission on Environmental Quality).

Resource Conservation and Recovery Act ("RCRA")

The federal RCRA and comparable state statutes govern the disposal of solid and hazardous wastes. In the event such wastes are generated in connection with our facilities, we are subject to regulatory requirements affecting the handling, transportation, treatment, storage and disposal of such wastes

Endangered Species Act

The Sabine Pass LNG terminal operations and the proposed liquefaction facilities may be restricted by requirements under the Endangered Species Act, which seeks to protect endangered or threatened animal, fish and plant species and designated habitats.

Market Factors and Competition

Sabine Pass LNG currently does not experience competition for its terminal capacity because the entire approximately 4.0 Bcf/d of regasification capacity that is available at the Sabine Pass LNG terminal has been fully contracted. If and when Sabine Pass LNG has to replace any TUAs, it will compete with other then-existing LNG terminals for customers.

The Liquefaction Project currently does not experience competition with respect to Train 1 through Train 4, and a portion of Train 5. Sabine Pass Liquefaction has entered into five fixed price, 20-year LNG SPAs that will utilize substantially all of the

liquefaction capacity available from these Trains. Each customer will be required to pay an escalating fixed fee for its annual contract quantity even if it elects not to purchase any LNG from us.

If and when Sabine Pass Liquefaction needs to replace any existing SPA or enter into new SPAs with respect to Train 5 and Train 6, Sabine Pass Liquefaction will compete on the basis of price per contracted volume of LNG with other LNG liquefaction projects throughout the world. Revenues associated with any incremental volumes of the Liquefaction Project, including those under the Cheniere Marketing SPA discussed above, will also be subject to market-based price competition.

Our ability to sell any seasonal quantities of LNG available from Train 1 through Train 4, develop additional Trains, or develop other new projects is subject to a broader array of market factors, including: changes in worldwide supply and demand for natural gas, LNG and substitute products; the relative prices for natural gas, crude oil and substitute products in North America and international markets; economic growth in developing countries; investment in energy infrastructure; the rate of fuel switching for power generation from coal, nuclear or oil to natural gas; and access to capital markets.

We expect global demand for natural gas and LNG to grow significantly as nations seek more abundant, reliable and environmentally cleaner fuel alternatives to oil and coal. Global demand for natural gas is projected by the International Energy Agency to grow by more than 24 Tcf between 2010 and 2020, fueled by the growth of emerging economies. Global demand for LNG is forecast to increase by 49%, or 5.7 Tcf, by 2020 and reach a total of 456 mmtpa, or 22.2 Tcf, by 2025. LNG is substantially more flexible than pipeline-delivered natural gas. As a result, the share of LNG in the global natural gas market is expected to increase as markets seek to improve security of supply by accessing a wide portfolio of producers that can readjust deliveries to meet the needs of changing markets.

While global natural gas consumption has been rising internationally, natural gas production in the United States has undergone a technological transformation that has resulted in a substantial increase in annual production capacity, decrease in the cost of production, and expansion of technically recoverable reserves.

Our ability to continue to develop new facilities in the United States will be driven in part by the continued success of the North American upstream natural gas sector in developing new reservoirs, continuing to drive down costs and producing higher valued condensates and natural gas liquids in conjunction with natural gas production. Any such facilities will compete with other international LNG export projects principally on a price basis. These projects generally require capital not only to build the marine, storage and liquefaction facilities, but also to drill wells and build processing and pipeline transportation infrastructure. Because we rely on the natural gas market and transportation infrastructure already existing in the United States, we generally require less capital expenditures than competing projects. Furthermore, because natural gas is purchased from the United States market at a Henry Hub related price, we can offer LNG for sale at an alternative price to crude oil prices, thereby providing customers with an opportunity to diversify their supply portfolios by geography and price index.

Subsidiaries

Our assets are generally held by or under our operating subsidiaries. We conduct most of our operations through these subsidiaries, including our operations relating to the development and operation of our LNG terminal business and the Liquefaction Project.

Employees and Labor Relations

We have no employees. We rely on our general partner to manage all aspects of the operation, maintenance and construction of the Sabine Pass LNG terminal, the Liquefaction Project and the conduct of our business. Because our general partner has no employees, it relies on subsidiaries of Cheniere to provide the personnel necessary to allow it to meet its management obligations to us, Sabine Pass LNG and Sabine Pass Liquefaction. As of February 13, 2013, Cheniere and its subsidiaries had 306 full-time employees, including 163 employees who directly supported the Sabine Pass LNG terminal operations and the Liquefaction Project. See Note 13—"Related Party Transactions" in our Notes to Consolidated Financial Statements for a discussion of these arrangements. Cheniere considers its current employee relations to be favorable.

Available Information

Our common units have been publicly traded since March 21, 2007, and are traded on the NYSE MKT under the symbol "CQP". Our principal executive offices are located at 700 Milam Street, Suite 800, Houston, Texas 77002, and our telephone number is (713) 375-5000. Our internet address is http://www.cheniereenergypartners.com. We provide public access to our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to these reports as soon as reasonably practicable after we electronically file those materials with, or furnish those materials to, the Securities and Exchange Commission ("SEC") under the Exchange Act. These reports may be accessed free of charge through our internet website. We make our website content available for informational purposes only. The website should not be relied upon for investment purposes and is not incorporated by reference into this Form 10-K.

We will also make available to any unitholder, without charge, copies of our Annual Report on Form 10-K as filed with the SEC. For copies of this, or any other filing, please contact: Cheniere Energy Partners, L.P, Investor Relations Department, 700 Milam Street, Suite 800, Houston, Texas 77002 or call (713) 562-5000. In addition, the public may read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E., Room 1580, Washington, D.C. 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an internet site (www.sec.gov) that contains reports and other information regarding issuers, like us, that file electronically with the SEC.

ITEM 1A. RISK FACTORS

Limited partner interests are inherently different from the capital stock of a corporation, although many of the business risks to which we are subject are similar to those that would be faced by a corporation engaged in a similar business. The following are some of the important factors that could affect our financial performance or could cause actual results to differ materially from estimates or expectations contained in our forward-looking statements. We may encounter risks in addition to those described below. Additional risks and uncertainties not currently known to us, or that we currently deem to be immaterial, may also impair or adversely affect our business, contracts, financial condition, operating results, cash flows, liquidity and prospects.

The risk factors in this report are grouped into the following categories:

| |

• | Risks Relating to Our Financial Matters; |

| |

• | Risks Relating to Our Business; |

| |

• | Risks Relating to Our Cash Distributions; |

| |

• | Risks Relating to an Investment in Us and Our Common Units; and |

| |

• | Risks Relating to Tax Matters. |

Risks Relating to Our Financial Matters

Our existing level of cash resources, negative operating cash flow and significant debt could cause us to have inadequate liquidity and could materially and adversely affect our business, financial condition and prospects.

As of December 31, 2012, we had $419.3 million of cash and cash equivalents and $364.9 million of restricted cash and cash equivalents, and we had $2.2 billion of total debt outstanding on a consolidated basis (before debt discounts). In addition, in February 2013, we issued an additional $1.5 billion of indebtedness to finance the capital costs in connection with the construction of Train 1 and Train 2. We incur significant interest expense relating to the assets at the Sabine Pass LNG terminal and Liquefaction Project, and we anticipate needing to incur substantial additional debt and issue equity to finance the construction of all six trains of the Liquefaction Project. Our ability to fund our capital expenditures and refinance our indebtedness will depend on our ability to access capital markets. Furthermore, our costs could increase or future borrowings or equity offerings may be unavailable to us or unsuccessful, which could cause us to be unable to pay or refinance our indebtedness or to fund our other liquidity needs.

We have not been profitable historically, and we have not had positive operating cash flow. Our ability to achieve profitability and generate positive operating cash flow in the future is subject to significant uncertainty.

We had net losses of $150.1 million and $31.0 million for the years ended December 31, 2012 and 2011, respectively. In addition, our net cash flow used in operating activities was $26.2 million for the year ended December 31, 2012. In the future, we may incur operating losses and experience negative operating cash flow. We may not be able to reduce costs, increase revenues, or reduce our debt service obligations sufficiently to maintain our cash resources, which could cause us to have inadequate liquidity to continue our business.

In addition, we will continue to incur significant capital and operating expenditures while we develop and construct the Liquefaction Project. We currently expect that we will not begin to receive cash flows from operations under any SPA until the end of 2015, at the earliest. Any delays beyond the expected development periods for Train 1 would prolong, and could increase the level of, our operating losses and negative operating cash flows. Our future liquidity may also be affected by the timing of construction financing availability in relation to the incurrence of construction costs and other outflows and by the timing of receipt of cash flows under SPAs in relation to the incurrence of project and operating expenses. Moreover, many factors (including factors beyond our control) could result in a disparity between liquidity sources and cash needs, including factors such as construction delays and breaches of agreements. Our ability to generate positive operating cash flow and achieve profitability in the future is dependent on our ability to successfully and timely complete the applicable Train.

In order to generate needed amounts of cash, we may sell equity or equity-related securities, including additional common units. Such sales could dilute our unitholders' proportionate indirect interests in our assets, business operations, Liquefaction Project and other projects, and could adversely affect the market price of our common units.

We have pursued and are pursuing a number of alternatives in order to generate needed amounts of cash, including potential issuances and sales of additional equity or equity-related securities by us. Such sales, in one or more transactions, could dilute our unitholders' proportionate indirect interests in our assets, business operations and proposed projects, including the Liquefaction Project. In addition, such sales, or the anticipation of such sales, could adversely affect the market price of our common units.

Our ability to generate needed amounts of cash is substantially dependent upon the performance by customers under long-term contracts that we have entered into, and we could be materially and adversely affected if any customer fails to perform its contractual obligations for any reason.

Our future results and liquidity are substantially dependent upon performance by Chevron and Total, each of which has entered into a TUA with Sabine Pass LNG and agreed to pay us approximately $125 million annually, and, upon satisfaction of the conditions precedent to payment thereunder, by BG, Gas Natural Fenosa, KOGAS, GAIL and Total, each of which has entered into an SPA with Sabine Pass Liquefaction and agreed to pay us approximately $723 million, $454 million, $548 million, $548 million and $314 million annually, respectively. We are dependent on each customer's continued willingness and ability to perform its obligations under its SPA. We are also exposed to the credit risk of any guarantor of these customers' obligations under their respective TUA or SPA in the event that we must seek recourse under a guaranty. If any customer fails to perform its obligations under its TUA or SPA, our business, contracts, financial condition, operating results, cash flow, liquidity and prospects could be materially and adversely affected, even if we were ultimately successful in seeking damages from that customer or its guarantor for a breach of the TUA or SPA.

Each of our customer contracts is subject to termination under certain circumstances.

Each of Sabine Pass LNG's long-term TUAs contains various termination rights. For example, each customer may terminate its TUA if the Sabine Pass LNG terminal experiences a force majeure delay for longer than 18 months, fails to redeliver a specified amount of natural gas in accordance with the customer's redelivery nominations or fails to accept and unload a specified number of the customer's proposed LNG cargoes. Sabine Pass LNG may not be able to replace these TUAs on desirable terms, or at all, if they are terminated.

Each of Sabine Pass Liquefaction's SPAs contain various termination rights allowing our customers to terminate their SPAs including, without limitation: (i) upon the occurrence of certain events of force majeure; (ii) if we fail to make available specified scheduled cargo quantities; (iii) delays in the commencement of commercial operations; and (iv) if the conditions precedent contained in the SPAs are not met or waived by specified dates. We may not be able to replace these SPAs on desirable terms, or at all, if they are terminated.

Our use of hedging arrangements may adversely affect our future results of operations or liquidity.

To reduce our exposure to fluctuations in the price, volume and timing risk associated with the purchase of natural gas, we use futures, swaps and option contracts traded or cleared on the Intercontinental Exchange and NYMEX, or over-the-counter options and swaps with other natural gas merchants and financial institutions. Hedging arrangements would expose us to risk of financial loss in some circumstances, including when:

| |

• | expected supply is less than the amount hedged; |

| |

• | the counterparty to the hedging contract defaults on its contractual obligations; or |

| |

• | there is a change in the expected differential between the underlying price in the hedging agreement and actual prices received. |

The use of derivatives also may require the posting of cash collateral with counterparties, which can impact working capital when commodity prices change.

The enactment of the Dodd-Frank Act could have an adverse impact on our ability to hedge risks associated with our business.

Congress adopted comprehensive financial reform legislation that establishes federal oversight and regulation of the OTC derivatives market and entities, such as us, that participate in that market. This legislation, known as the Dodd-Frank Wall Street Reform and Consumer Protection Act (the "Dodd-Frank Act"), requires the Commodities Futures Trading Commission (the

"CFTC") and the SEC to promulgate certain rules and regulations, including relating to the regulation of certain swaps entities, the clearing of certain swaps, and the reporting and recordkeeping of swaps, and gave the CFTC the authority to establish position limits. Although the CFTC established position limits on certain core futures and equivalent swaps contracts for physical commodities, including natural gas, with exceptions for certain bona fide hedging transactions, those limits were vacated by federal district court in September 2012 and will not go into effect unless and until the CFTC prevails on appeal of this ruling or issues and finalizes revised rules.

In December 2012, the CFTC published final rules regarding mandatory clearing of certain interest rate swaps and certain index credit default swaps and setting compliance dates for different categories of market participants, the earliest of which is March 2013. The CFTC has not yet proposed any rules requiring the clearing of any other classes of swaps, including physical commodity swaps. Although we expect to qualify for the end-user exception from the clearing requirement for our swaps, mandatory clearing requirements applicable to other market participants, such as swap dealers, may change the cost and availability of the swaps that we use for hedging. In addition, for uncleared swaps, the CFTC or other regulators may require our counterparties to require that we enter into credit support documentation and/or post initial and variation margin as collateral; however, the proposed margin rules are not yet final, and therefore the application of those provisions to us is uncertain at this time. The financial reform legislation may also cause our derivatives counterparties to spin off some of their derivatives activities to a separate entity, which may not be as creditworthy as the current counterparty. The new legislation and any new regulations could significantly increase the cost of derivative contracts (including through requirements to post collateral which could adversely affect our available liquidity), materially alter the terms of derivative contracts, reduce the availability of derivatives to protect against risks that we encounter, reduce our ability to monetize or restructure our existing derivative contracts, and increase our exposure to less creditworthy counterparties.

Risks Relating to Our Business

Operation of the Sabine Pass LNG terminal, the Liquefaction Project and other facilities that we may construct involves significant risks.

As more fully discussed in these Risk Factors, the Sabine Pass LNG terminal, the Liquefaction Project and our other existing and proposed facilities face operational risks, including the following:

| |

• | the facilities' performing below expected levels of efficiency; |

| |

• | breakdown or failures of equipment; |

| |

• | operational errors by vessel or tug operators; |

| |

• | operational errors by us or any contracted facility operator; |

| |

• | weather-related interruptions of operations. |

We may not be successful in implementing our proposed business strategy to provide liquefaction capabilities at the Sabine Pass LNG terminal adjacent to the existing regasification facilities.

The Liquefaction Project will require very significant financial resources, which may not be available on terms reasonably acceptable to us or at all. Our SPAs with KOGAS, GAIL and Total contain certain conditions precedent, including, but not limited to, receiving regulatory approvals, securing necessary financing arrangements and making a final investment decision to construct Train 3, Train 4 or Train 5, respectively. If these conditions are not met by December 31, 2013 with respect to KOGAS and GAIL and June 30, 2015 with respect to Total, the applicable party may terminate the respective SPA. In addition, if, by June 30, 2013, we have not made a positive final investment decision (i) to construct Train 3, either party may cancel BG's annual contract quantity of 34.0 million MMBtu commencing upon the date of first commercial delivery for Train 3 and the 33.5 million MMBtu commencing upon the date of first commercial delivery for Train 4 and (ii) to construct Train 4, either party may cancel BG's annual contract quantity of 33.5 million MMBtu commencing upon the date of first commercial delivery for Train 4.

It will take several years to construct our proposed liquefaction facilities, and we do not expect Train 1 to produce LNG until the end of 2015, at the earliest. Even if successfully constructed, our proposed liquefaction facilities would be subject to the operating risks described herein. Accordingly, there are many risks associated with the Liquefaction Project, and if we are not

successful in implementing our business strategy, we may not be able to generate cash flows, which could have a material adverse impact on our business, contracts, financial condition, operating results, cash flow, liquidity and prospects.

Cost overruns and delays in the completion of one or more Trains, as well as difficulties in obtaining sufficient financing to pay for such costs and delays, could have a material adverse effect on our business, contracts, financial condition, operating results, cash flow, liquidity and prospects.

The actual construction costs of the Trains may be significantly higher than our current estimates as a result of many factors, including change orders under existing or future engineering, procurement and construction contracts. We do not have any prior experience in constructing liquefaction facilities, and no liquefaction facilities have been constructed and placed in service in the United States in over 40 years. As construction progresses, we may decide or be forced to submit change orders to our contractor that could result in longer construction periods, higher construction costs or both.

Key factors that may affect the timing of, cost of, or our ability to complete, one or more of our proposed Trains include, but are not limited to:

| |

• | the issuance and/or continued availability of necessary permits, licenses and approvals from governmental agencies and third parties as are required to construct and operate our proposed liquefaction facilities; |

| |

• | the availability of sufficient financing on reasonable terms, or at all; |

| |

• | our ability to satisfy the conditions precedent in SPAs with customers by specified dates; |

| |

• | our ability to enter into additional satisfactory agreements with contractors and to maintain good relationships with these contractors in order to construct our proposed liquefaction facilities within the expected cost parameters, and the ability of those contractors to perform their obligations under the contracts and to maintain their creditworthiness; |

| |

• | shortages of materials or delays in delivery of materials; |

| |

• | local and general economic conditions; |

| |

• | catastrophes, such as explosions, fires and product spills; |

| |

• | resistance in the local community to the project to add liquefaction capabilities at the Sabine Pass LNG terminal adjacent to the existing regasification facilities; |

| |

• | the ability to attract sufficient skilled and unskilled labor, increases in the level of labor costs and the existence of any labor disputes; and |

| |

• | weather conditions, such as hurricanes. |

Delays in the construction of one or more Trains beyond the estimated development periods, as well as change orders to the EPC Contracts with Bechtel or any future engineering, procurement and construction contract related to additional Trains, could increase the cost of completion beyond the amounts that we estimate, which could require us to obtain additional sources of financing to fund our operations until the Liquefaction Project is constructed (which could cause further delays). Our ability to obtain financing that may be needed to provide additional funding to cover increased costs will depend, in part, on factors beyond our control. Accordingly, we may not be able to obtain financing on terms that are acceptable to us, or at all. Even if we are able to obtain financing, we may have to accept terms that are disadvantageous to us or that may have a material adverse effect on our current or future business, contracts, financial condition, operating results, cash flow, liquidity and prospects.

Delays in the completion of one or more Trains could lead to reduced revenues or termination of one or more of the SPAs by our counterparties.

Any delay in completion of a Train may prevent us from commencing operations when anticipated, which could cause a delay in the receipt of revenues projected therefrom or cause a loss of one or more customers in the event of significant delays. As a result, any significant construction delay, whatever the cause, could have a material adverse effect on our business, contracts, financial condition, operating results, cash flow, liquidity and prospects.

Our ability to complete development of additional Trains will be contingent on our ability to obtain additional funding. If we are unable to obtain sufficient funding, we may be unable to implement or complete our business plan and our business may ultimately be unsuccessful.

We will require significant additional funding to be able to commence construction of Train 3 through Train 6, which we may not be able to obtain at a cost that results in positive economics, or at all. The inability to achieve acceptable funding may cause a delay in development of additional Trains, and we may never be able to complete the development of our business plan. Even if we are able to obtain funding, the funding may be inadequate to cover any increases in costs or delays in completion of the applicable Train, which may cause a delay in the receipt of revenues projected therefrom or cause a loss of one or more customers in the event of significant delays. As a result, any significant construction delay, whatever the cause, could have a material adverse effect on our business, contracts, financial condition, operating results, cash flow, liquidity and prospects.

To maintain the cryogenic readiness of the Sabine Pass LNG terminal, Sabine Pass LNG may need to purchase and process LNG. Sabine Pass LNG's TUA customers have the obligation to procure LNG if necessary for the Sabine Pass LNG terminal to maintain its cryogenic state. If they fail to do so, Sabine Pass LNG may need to procure such LNG.

Sabine Pass LNG needs to maintain the cryogenic readiness of the Sabine Pass LNG terminal. Together with Sabine Pass Liquefaction, the two third-party TUA customers have the obligation to maintain minimum inventory levels, and under certain circumstances, to procure LNG to maintain the cryogenic readiness of the terminal. In the event that aggregate minimum inventory levels are not maintained, Sabine Pass LNG has the right to procure a cryogenic readiness cargo, and to the extent that the TUA customers have failed to maintain their minimum inventory levels, be reimbursed by each TUA customer for their allocable share of the LNG acquisition costs. If Sabine Pass LNG is not able to obtain financing on acceptable terms, it will need to maintain sufficient working capital for such a purchase until it receives reimbursement for the allocable costs of the LNG from its TUA customers or sells the regasified LNG. Sabine Pass LNG may also bear the commodity price and other risks of purchasing LNG, holding it in its inventory for a period of time and selling the regasified LNG.

Sabine Pass LNG may be required to purchase natural gas to provide fuel at the Sabine Pass LNG terminal, which would increase operating costs and could have a material adverse effect on our results of operations.

Sabine Pass LNG's TUAs provide for an in-kind deduction of 2% of the LNG delivered to the Sabine Pass LNG terminal, which it uses primarily as fuel for revaporization and self-generated power and to cover natural gas unavoidably lost at the facility. There is a risk that this 2% in-kind deduction will be insufficient for these needs and that Sabine Pass LNG will have to purchase additional natural gas from third parties. Sabine Pass LNG will bear the cost and risk of changing prices for any such fuel.

Hurricanes or other disasters could result in an interruption of our operations, a delay in the completion of the Liquefaction Project, higher construction costs, and the deferral of the dates on which payments are due to Sabine Pass Liquefaction under the SPAs, all of which could adversely affect us.

In August and September of 2005, Hurricanes Katrina and Rita damaged coastal and inland areas located in Texas, Louisiana, Mississippi and Alabama, resulting in the temporary suspension of construction of the Sabine Pass LNG terminal. In September 2008, Hurricane Ike struck the Texas and Louisiana coast, and the Sabine Pass LNG terminal experienced minor damage.

Future storms and related storm activity and collateral effects, or other disasters such as explosions, fires, floods or accidents, could result in damage to, or interruption of operations at, the Sabine Pass LNG terminal and related infrastructure, as well as delays or cost increases in the construction and the development of the Liquefaction Project and related infrastructure. If there are changes in the global climate, storm frequency and intensity may increase; should it result in rising seas, our coastal operations may be impacted.

Failure to obtain and maintain approvals and permits from governmental and regulatory agencies with respect to the design, construction and operation of our facilities could impede operations and construction and could have a material adverse effect on us.

The design, construction and operation of LNG terminals, including the Liquefaction Project, and other facilities, and the import and export of LNG, are highly regulated activities. The FERC's approval under Section 3 of the NGA, as well as several other material governmental and regulatory approvals and permits, are required in order to construct and operate an LNG facility. Although the FERC has issued an order under the Section 3 of the NGA authorizing the siting, construction and operation of four Trains, the FERC order requires us to obtain certain additional approvals in conjunction with ongoing construction and operations of our proposed liquefaction facilities. Authorizations obtained from other federal and state regulatory agencies also contain ongoing conditions, and additional approval and permit requirements may be imposed. We have no control over the outcome of

the review and approval process. We do not know whether or when any such approvals or permits can be obtained, or whether or not any existing or potential interventions or other actions by third parties will interfere with our ability to obtain and maintain such permits or approvals. If we are unable to obtain and maintain the necessary approvals and permits, we may not be able to recover our investment in our projects. There is no assurance that we will obtain and maintain these governmental permits, approvals and authorizations, or that we will be able to obtain them on a timely basis, and failure to obtain and maintain any of these permits, approvals or authorizations could have a material adverse effect on our business, financial condition, operating results, liquidity and prospects.

We are entirely dependent on Cheniere, including employees of Cheniere and its subsidiaries, for key personnel, and a loss of key personnel could have a material adverse effect on our business.

As of February 12, 2013, Cheniere and its subsidiaries had 306 full-time employees, including 163 employees who directly supported the Sabine Pass LNG terminal operations and Liquefaction Project construction. We have contracted with subsidiaries of Cheniere to provide the personnel necessary for the operation, maintenance and management of the Sabine Pass LNG terminal and construction of the Liquefaction Project. We face competition for these highly skilled employees in the immediate vicinity of the Sabine Pass LNG terminal and more generally from the Gulf Coast hydrocarbon processing and construction industries. A shortage in the labor pool of skilled workers or other general inflationary pressures or changes in applicable laws and regulations could make it more difficult to attract and retain personnel and could require an increase in the wage and benefits packages that are offered, thereby increasing our operating costs.

Our general partner's executive officers are officers and employees of Cheniere and its affiliates. We do not maintain key person life insurance policies on any personnel, and our general partner does not have any employment contracts or other agreements with key personnel binding them to provide services for any particular term. The loss of the services of any of these individuals could have a material adverse effect on our business. In addition, our future success will depend in part on our general partner's ability to engage, and Cheniere's ability to attract and retain, additional qualified personnel.

We have numerous contractual and commercial relationships, and conflicts of interest, with Cheniere and its affiliates, including Cheniere Marketing.

We have agreements to compensate and to reimburse expenses of affiliates of Cheniere. In addition, Cheniere Investments has entered into a VCRA with Cheniere Marketing, under which Cheniere Marketing will be able to derive economic benefits to the extent it assists Cheniere Investments in commercializing Cheniere Investments' access to capacity at the Sabine Pass LNG terminal through its TURA with Sabine Pass Liquefaction, which has a TUA with Sabine Pass LNG. In addition, Cheniere Marketing has entered into an SPA to purchase, at its option, any excess LNG produced that is not committed to non-affiliate parties, for up to a maximum of 104,000,000 MMBtu per annum produced from Train 1 through Train 4. All of these agreements involve conflicts of interest between us, on the one hand, and Cheniere and its other affiliates, on the other hand.

We expect that there will be additional agreements or arrangements with Cheniere and its affiliates, including future transportation, interconnection and gas balancing agreements with one or more Cheniere-affiliated natural gas pipelines as well as other agreements and arrangements that cannot now be anticipated. In those circumstances where additional contracts with Cheniere and its affiliates may be necessary or desirable, additional conflicts of interest will be involved.

We are dependent on Cheniere and its affiliates to provide services to us. If Cheniere or its affiliates are unable or unwilling to perform according to the negotiated terms and timetable of their respective agreement for any reason or terminates their agreement, we would be required to engage a substitute service provider. This could result in a significant interference with operations and increased costs.

We are dependent on Bechtel and other contractors for the successful completion of the Liquefaction Project.

Timely and cost-effective completion of the Liquefaction Project in compliance with agreed specifications is central to our business strategy and is highly dependent on Bechtel's and our other contractors' performance under their agreements. Bechtel's and our other contractors' ability to perform successfully under their agreements is dependent on a number of factors, including their ability to:

| |

• | design and engineer each Train to operate in accordance with specifications; |